Question: please show in excel. please also show the formulas you used to get the answer. 5) Assume the security returns are generated by a single

please show in excel. please also show the formulas you used to get the answer.

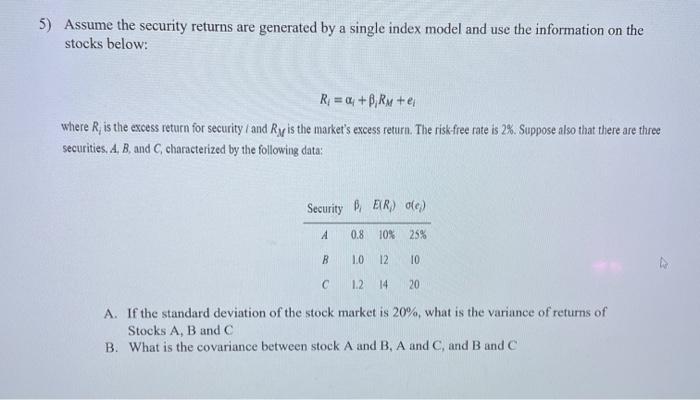

5) Assume the security returns are generated by a single index model and use the information on the stocks below: R = + B, Re where R, is the excess return for security / and Ry is the market's excess return. The risk-free rate is 2%. Suppose also that there are three Securities. A, B and C, characterized by the following data: Security BER) Oc) A 0.8 10% 25% B 10 12 10 1.2 14 20 A. If the standard deviation of the stock market is 20%, what is the variance of returns of Stocks A, B and C B. What is the covariance between stock A and B, A and C, and B and C

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock