Question: Please show steps and formulas used. Please do not use excel or other programs. Thank you. Problem 4. We have a financial market with many

Please show steps and formulas used. Please do not use excel or other programs. Thank you.

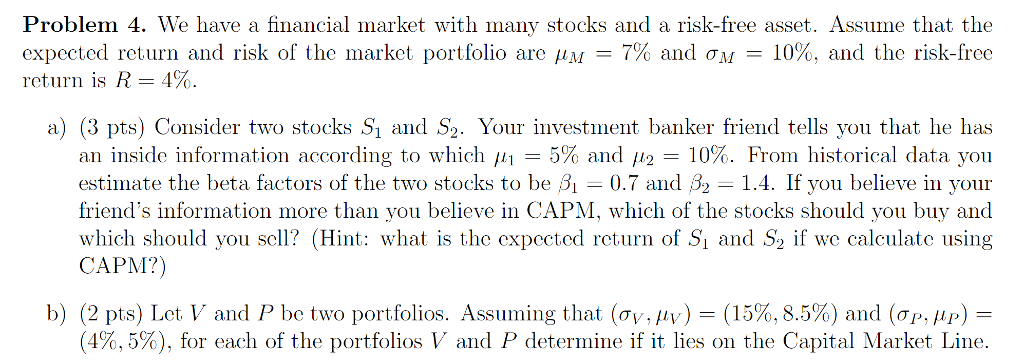

Problem 4. We have a financial market with many stocks and a risk-free asset. Assume that the expected return and risk of the market portfolio are ,Al-7% and M-- 10%, and the risk-free return is R 4%. a) (3 pts) Consider two stocks Si and S2. Your investment banker friend tells you that he has an inside information according to which ,11-5% and 2 10%. From historical data you estimate the beta factors of the two stocks to be 0.7 and 2 1.4. If you believe in your friend's information more than you believe in CAPM, which of the stocks should you buy and which should you sell? (Hint: what is the expected return of Si and S2 if we calculate using CAPM?) b) (2 pts) Let V and P be tw o portfolios. Assuming that (, )-(15%, 8.5%) and CP ,,n ) (49.5% , for each of the portfolios V and P determine if it lies on the Capital Market Line

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts