Question: Please show steps on how to solve B and C. A pension fund manager is considering three mutual funds. The first is a stock fund,

Please show steps on how to solve B and C.

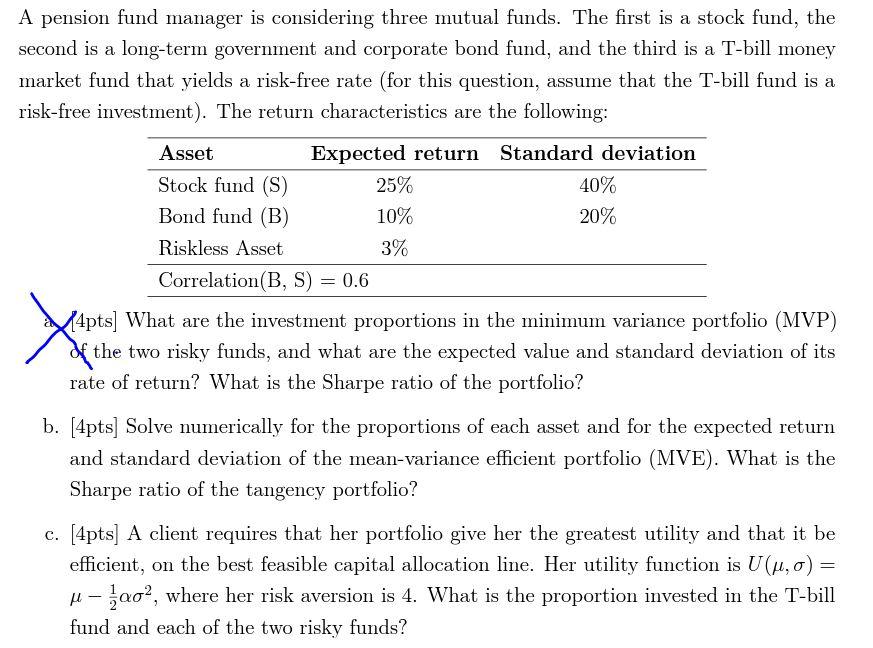

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a risk-free rate (for this question, assume that the T-bill fund is a risk-free investment). The return characteristics are the following: 4pts] What are the investment proportions in the minimum variance portfolio (MVP) rate of return? What is the Sharpe ratio of the portfolio? b. [4pts] Solve numerically for the proportions of each asset and for the expected return and standard deviation of the mean-variance efficient portfolio (MVE). What is the Sharpe ratio of the tangency portfolio? c. [4pts] A client requires that her portfolio give her the greatest utility and that it be efficient, on the best feasible capital allocation line. Her utility function is U(,)= 212, where her risk aversion is 4 . What is the proportion invested in the T-bill fund and each of the two risky funds

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts