Question: Please show steps to get the correct answer as the steps above did not yield the correct answer. (the answers start at b. but that

Please show steps to get the correct answer as the steps above did not yield the correct answer. (the answers start at b. but that was actually a. and so forth)

Please show steps to get the correct answer as the steps above did not yield the correct answer. (the answers start at b. but that was actually a. and so forth)

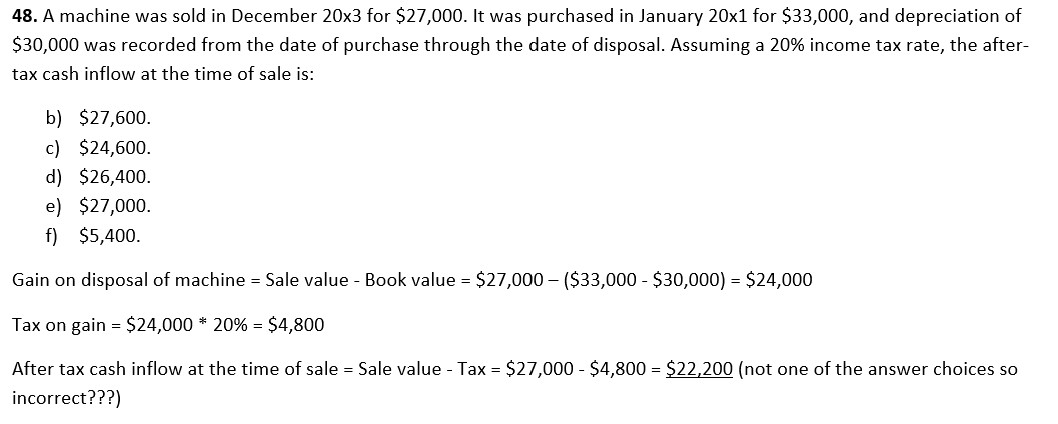

48. A machine was sold in December 20x3 for $27,000. It was purchased in January 20x1 for $33,000, and depreciation of $30,000 was recorded from the date of purchase through the date of disposal. Assuming a 20% income tax rate, the after- tax cash inflow at the time of sale is: b) $27,600. c) $24,600. d) $26,400. e) $27,000. f) $5,400. Gain on disposal of machine = Sale value - Book value = $27,000 ($33,000 - $30,000) = $24,000 Tax on gain = $24,000 * 20% = $4,800 After tax cash inflow at the time of sale = Sale value - Tax = $27,000 - $4,800 = $22,200 (not one of the answer choices so incorrect???)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts