Question: please show work 1. Show your work with the data below. (50 points) Calculate the call option value(Ve) of a call option with Black-Schokes Option

please show work

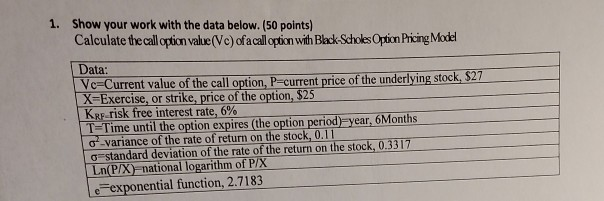

1. Show your work with the data below. (50 points) Calculate the call option value(Ve) of a call option with Black-Schokes Option Pricing Model Data: Vc Current value of the call option, P-current price of the underlying stock, $27 X-Exercise, or strike, price of the option, $25 KRF risk free interest rate, 6 % T-Time until the option expires (the option period) year, 6Months a-variance of the rate of return on the stock, 0.11 a standard deviation of the rate of the return on the stock, 0.3317 Ln(P/X)=national logarithm of P/X exponential function, 2.7183

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock