Question: Please solve all subparts. Problem 3 Binomial Pricing Model. Suppose that a a stock is currently selling for So = $150 and next year will

Please solve all subparts.

Please solve all subparts.

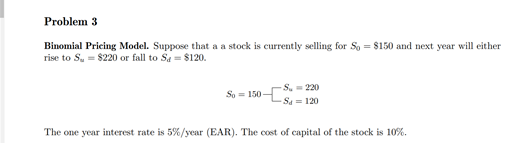

Problem 3 Binomial Pricing Model. Suppose that a a stock is currently selling for So = $150 and next year will either rise to S = $220 or fall to Sc = $120. So 150 S=220 SA = 120 The one year interest rate is 5%/year (EAR). The cost of capital of the stock is 10%. $220. (a) (5 points) Compute the risk-neutral probability of an up movement to have S; ) Solution: (b) (5 points) Compute the price of a call option struck at K$200. Solution: : (c) (5 points) Find a portfolio of the call and the stock that is riskless. Solution: : (d) (5 points) What is the expected return of the call? ) () Solution: Problem 3 Binomial Pricing Model. Suppose that a a stock is currently selling for So = $150 and next year will either rise to S = $220 or fall to Sc = $120. So 150 S=220 SA = 120 The one year interest rate is 5%/year (EAR). The cost of capital of the stock is 10%. $220. (a) (5 points) Compute the risk-neutral probability of an up movement to have S; ) Solution: (b) (5 points) Compute the price of a call option struck at K$200. Solution: : (c) (5 points) Find a portfolio of the call and the stock that is riskless. Solution: : (d) (5 points) What is the expected return of the call? ) () Solution

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts