Question: please use excel for all part for this problem! this is the data A. Plot historical prices for the six assets on the same line

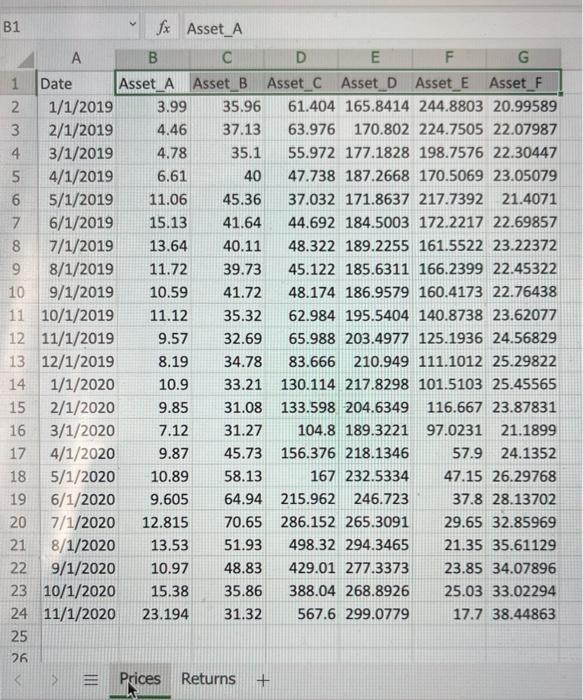

A. Plot historical prices for the six assets on the same line chart. B. Compute returns on all the assets (Asset A-F) in the Returns tab. C.A portfolio allocates 20% to Asset A 20% to ETF Asset_B, 20% to Asset C and 40% to Asset_D. Compute the mean, standard deviation, skewness, kurtosis, and Sharpe Ratio of this portfolio and the four assets (A, B, C, and D). Sharpe Ratio is defined as the ratio of mean to standard deviation (assuming risk free rate is zero). D. A 130/30 trading strategy means shorting an asset up to 30% of the portfolio value and then taking the funds to long positions on other assets. Considera 130/30 portfolio that is 50% Asset A, 30% Asset_8, 50% Asset Cand -30% Asset D. Compute the mean, standard deviation, skewness, and Sharpe Ratio of this portfolio Compare this portfolio to the one in Question C, what do you observe? E. Regress Asset A on Asset D. Asset_Bon Asset_D, and Asset Con Asset D and draw the following three scatter plots: Asset A vs Asset D. Asset B vs Asset D. Asset C vs Asset D. Given that Asset_Dis an ETF tracking the technology sector, which asset is more likely to be a technology stock? Why? F. What are your observations from Question E? Are the alphas and betas from the regressions in Question significant? Report the alphas and betas after taking the statistical significance into consideration G. Test if the portfolio return in Question is significant? Why? H. Test if the portfolio return in Question is equal to 1967 (a) write out the null and alternative hypothesis. (b) Compute the test statistic (0) Should she reject or fall to reject the null hypothesis? 1. Considering Asset E and Asset F. Which asset provides a better hedge to the portfolio in Question C? Test and explain why. Test whether Asset A and Asset B are correlated fi am telling you one is an ETF tracking bitcoin prices, and the other one is an ETF tracking avocado prices, can you provide a rationale to explain their relationship. B1 fx Asset_A A B D E G 1 Date Asset_A Asset B Asset_C Asset D Asset E Asset F 2 1/1/2019 3.99 35.96 61.404 165.8414 244.8803 20.99589 3 2/1/2019 4.46 37.13 63.976 170.802 224.7505 22.07987 4 3/1/2019 4.78 35.1 55.972 177.1828 198.7576 22.30447 5 4/1/2019 6.61 40 47.738 187.2668 170.5069 23.05079 6 5/1/2019 11.06 45.36 37.032 171.8637 217.7392 21.4071 7 6/1/2019 15.13 41.64 44.692 184.5003 172.2217 22.69857 8 7/1/2019 13.64 40.11 48.322 189.2255 161.5522 23.22372 9 8/1/2019 11.72 39.73 45.122 185.6311 166.2399 22.45322 10 9/1/2019 10.59 41.72 48.174 186.9579 160.4173 22.76438 11 10/1/2019 11.12 35.32 62.984 195.5404 140.8738 23.62077 12 11/1/2019 9.57 32.69 65.988 203.4977 125.1936 24.56829 13 12/1/2019 8.19 34.78 83.666 210.949 111.1012 25.29822 14 1/1/2020 10.9 33.21 130.114 217.8298 101.5103 25.45565 15 2/1/2020 9.85 31.08 133.598 204.6349 116.667 23.87831 3/1/2020 7.12 31.27 104.8 189.3221 97.0231 21.1899 17 4/1/2020 9.87 45.73 156.376 218.1346 57.9 24.1352 18 5/1/2020 10.89 58.13 167 232.5334 47.15 26.29768 19 6/1/2020 9.605 64.94 215.962 246.723 37.8 28.13702 20 7/1/2020 12.815 70.65 286.152 265.3091 29.65 32.85969 21 8/1/2020 13.53 51.93 498.32 294.3465 21.35 35.61129 22 9/1/2020 10.97 48.83 429.01 277.3373 23.85 34.07896 23 10/1/2020 15.38 35.86 388.04 268.8926 25.03 33.02294 24 11/1/2020 23.194 31.32 567.6 299.0779 17.7 38.44863 25 26 Prices Returns + Calculation Mode: Automatic Workbook Static A. Plot historical prices for the six assets on the same line chart. B. Compute returns on all the assets (Asset A-F) in the Returns tab. C.A portfolio allocates 20% to Asset A 20% to ETF Asset_B, 20% to Asset C and 40% to Asset_D. Compute the mean, standard deviation, skewness, kurtosis, and Sharpe Ratio of this portfolio and the four assets (A, B, C, and D). Sharpe Ratio is defined as the ratio of mean to standard deviation (assuming risk free rate is zero). D. A 130/30 trading strategy means shorting an asset up to 30% of the portfolio value and then taking the funds to long positions on other assets. Considera 130/30 portfolio that is 50% Asset A, 30% Asset_8, 50% Asset Cand -30% Asset D. Compute the mean, standard deviation, skewness, and Sharpe Ratio of this portfolio Compare this portfolio to the one in Question C, what do you observe? E. Regress Asset A on Asset D. Asset_Bon Asset_D, and Asset Con Asset D and draw the following three scatter plots: Asset A vs Asset D. Asset B vs Asset D. Asset C vs Asset D. Given that Asset_Dis an ETF tracking the technology sector, which asset is more likely to be a technology stock? Why? F. What are your observations from Question E? Are the alphas and betas from the regressions in Question significant? Report the alphas and betas after taking the statistical significance into consideration G. Test if the portfolio return in Question is significant? Why? H. Test if the portfolio return in Question is equal to 1967 (a) write out the null and alternative hypothesis. (b) Compute the test statistic (0) Should she reject or fall to reject the null hypothesis? 1. Considering Asset E and Asset F. Which asset provides a better hedge to the portfolio in Question C? Test and explain why. Test whether Asset A and Asset B are correlated fi am telling you one is an ETF tracking bitcoin prices, and the other one is an ETF tracking avocado prices, can you provide a rationale to explain their relationship. B1 fx Asset_A A B D E G 1 Date Asset_A Asset B Asset_C Asset D Asset E Asset F 2 1/1/2019 3.99 35.96 61.404 165.8414 244.8803 20.99589 3 2/1/2019 4.46 37.13 63.976 170.802 224.7505 22.07987 4 3/1/2019 4.78 35.1 55.972 177.1828 198.7576 22.30447 5 4/1/2019 6.61 40 47.738 187.2668 170.5069 23.05079 6 5/1/2019 11.06 45.36 37.032 171.8637 217.7392 21.4071 7 6/1/2019 15.13 41.64 44.692 184.5003 172.2217 22.69857 8 7/1/2019 13.64 40.11 48.322 189.2255 161.5522 23.22372 9 8/1/2019 11.72 39.73 45.122 185.6311 166.2399 22.45322 10 9/1/2019 10.59 41.72 48.174 186.9579 160.4173 22.76438 11 10/1/2019 11.12 35.32 62.984 195.5404 140.8738 23.62077 12 11/1/2019 9.57 32.69 65.988 203.4977 125.1936 24.56829 13 12/1/2019 8.19 34.78 83.666 210.949 111.1012 25.29822 14 1/1/2020 10.9 33.21 130.114 217.8298 101.5103 25.45565 15 2/1/2020 9.85 31.08 133.598 204.6349 116.667 23.87831 3/1/2020 7.12 31.27 104.8 189.3221 97.0231 21.1899 17 4/1/2020 9.87 45.73 156.376 218.1346 57.9 24.1352 18 5/1/2020 10.89 58.13 167 232.5334 47.15 26.29768 19 6/1/2020 9.605 64.94 215.962 246.723 37.8 28.13702 20 7/1/2020 12.815 70.65 286.152 265.3091 29.65 32.85969 21 8/1/2020 13.53 51.93 498.32 294.3465 21.35 35.61129 22 9/1/2020 10.97 48.83 429.01 277.3373 23.85 34.07896 23 10/1/2020 15.38 35.86 388.04 268.8926 25.03 33.02294 24 11/1/2020 23.194 31.32 567.6 299.0779 17.7 38.44863 25 26 Prices Returns + Calculation Mode: Automatic Workbook Static

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts