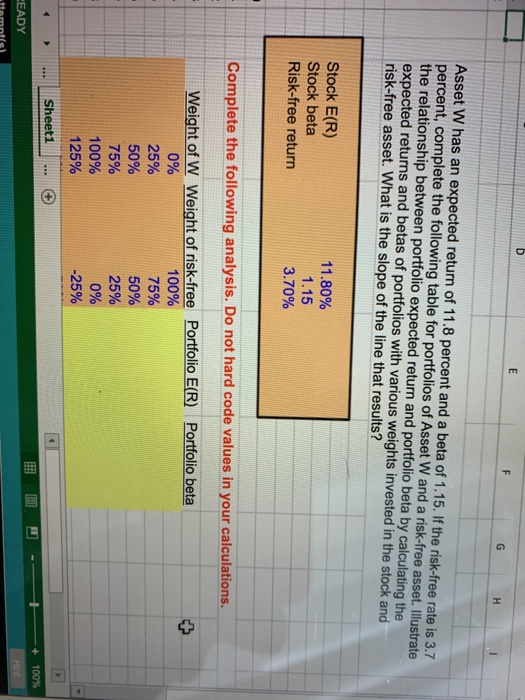

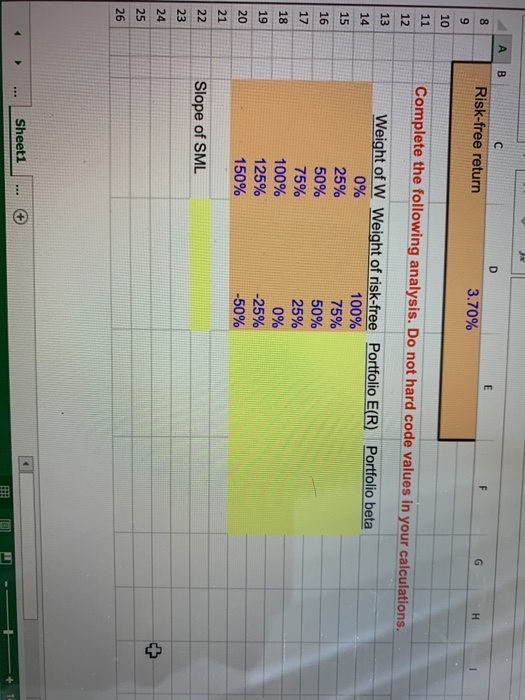

Question: please wirte the specific steps in excle, like = A1-A2-A3. Thanks D E F G H Asset W has an expected return of 11.8 percent

please wirte the specific steps in excle, like = A1-A2-A3. Thanks

please wirte the specific steps in excle, like = A1-A2-A3. ThanksD E F G H Asset W has an expected return of 11.8 percent and a beta of 1.15. If the risk-free rate is 3.7 percent, complete the following table for portfolios of Asset W and a risk-free asset. Illustrate the relationship between portfolio expected return and portfolio beta by calculating the expected returns and betas of portfolios with various weights invested in the stock and risk-free asset. What is the slope of the line that results? Stock E(R) Stock beta Risk-free return 11.80% 1.15 3.70% Complete the following analysis. Do not hard code values in your calculations. Weight of W Weight of risk-free Portfolio E(R) Portfolio beta 0% 100% 25% 75% 50% 50% 75% 25% 100% 0% 125% -25% Sheet1 . + 100% EADY A B D 8 E Risk-free return G 3.70% H 9 10 11 Complete the following analysis. Do not hard code values in your calculations. 12 13 14 15 16 Weight of W Weight of risk-free Portfolio E(R) Portfolio beta 0% 100% 25% 75% 50% 50% 75% 25% 100% 0% 125% -25% 150% -50% 17 18 19 20 21 22 Slope of SML 23 24 25 26 Sheet1 *** + ER

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts