Question: Pls only answer if able to fully ans the questions, Pls also give details workings Question 2 R18 Watch Limited manufactures wrist watches for various

Pls only answer if able to fully ans the questions, Pls also give details workings

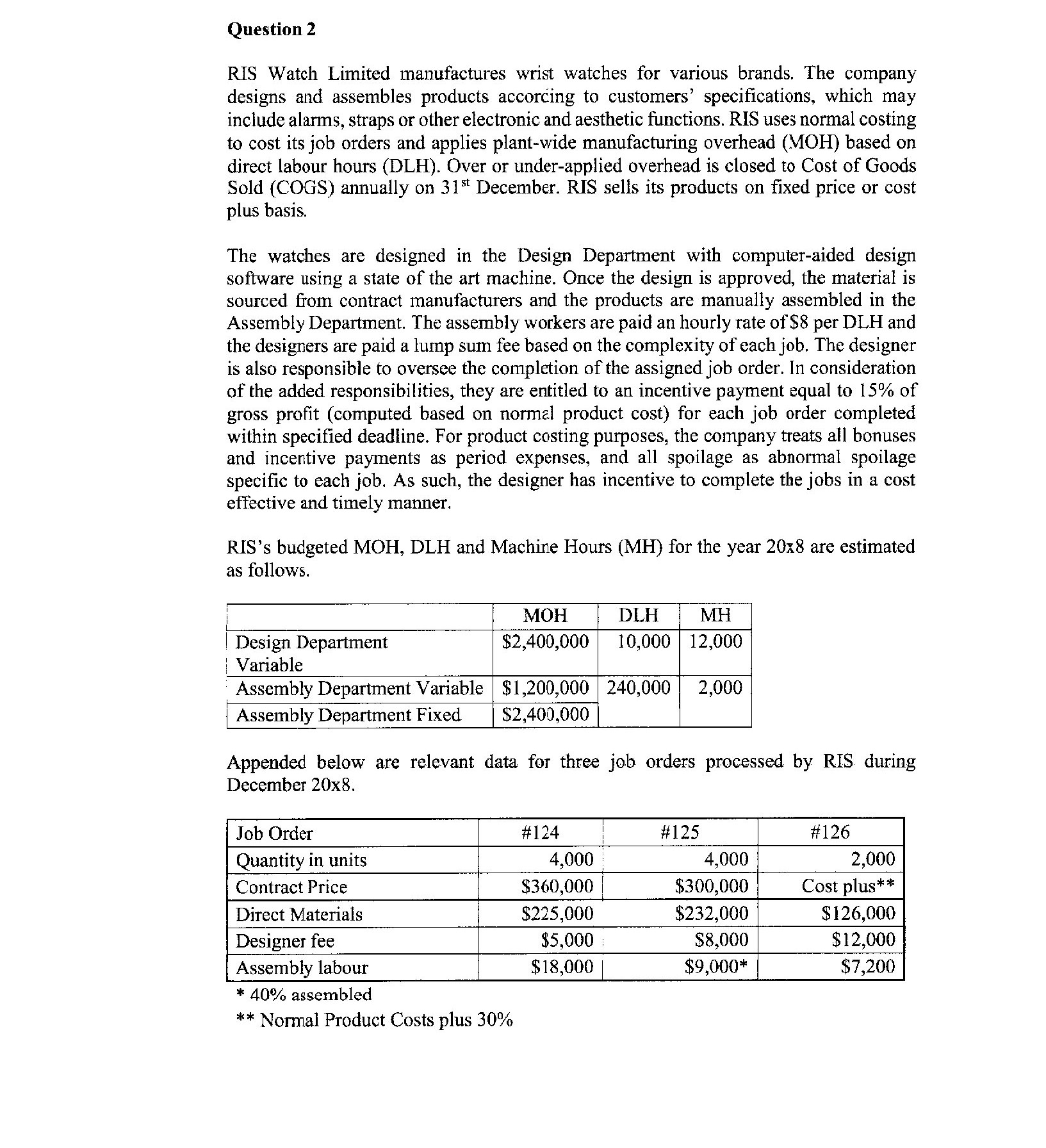

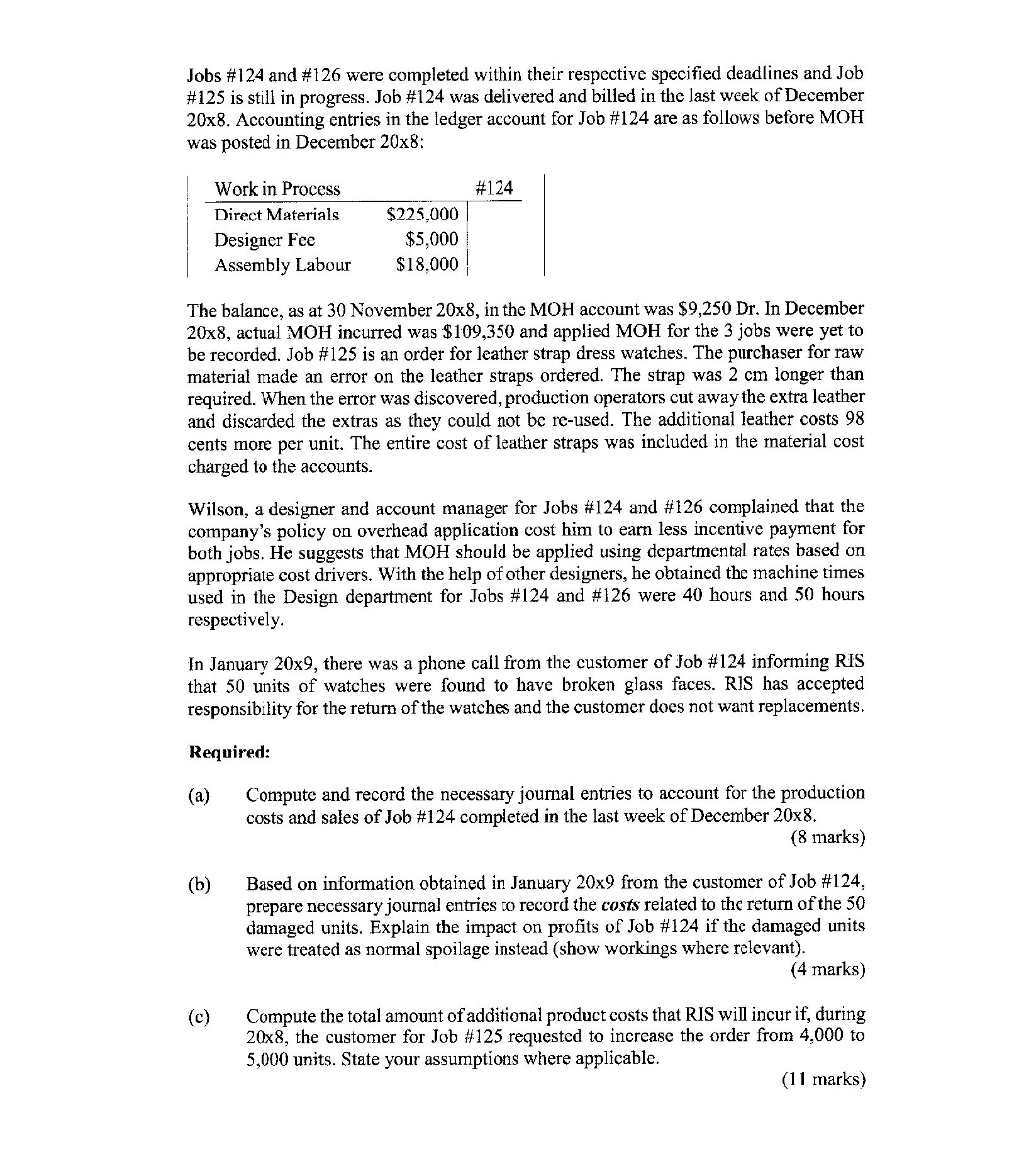

Question 2 R18 Watch Limited manufactures wrist watches for various brands. The company designs and assembles products according to customers' specications, which may include alarms, straps or other electronic and aesthetic functions. RIS uses normal costing to cost its job orders and applies plantwide manufacturing overhead (MOH) based on direct labour hours (DLH). Over or under-applied overhead is closed to Cost of Goods Sold (COGS) annually on 31St December. RIS sells its products on xed price or cost plus basis. The watches are designed in the Design Department with computer-aided design software using a state of the art machine. Once the design is approved, the material is sourced from contract manufacturers and the products are manually assembled in the Assembly Department. The assembly workers are paid an hourly rate of $8 per DLH and the designers are paid a lump sum fee based on the complexity of each job. The designer is also responsible to oversee the completion of the assigned job order. In consideration of the added responsibilities, they are entitled to an incentive payment equal to 15% of gross profit (computed based on normai product cost} for each job order completed within specied deadline. For product costing purposes, the company treats all bonuses and incentive payments as period expenses, and all spoilage as abnormal spoilage specic to each job. As such, the designer has incentive to complete the jobs in a cost effective and timely manner. RIS's budgeted MOH, DLH and Machine Hours (MH) for the year 20x8 are estimated as follows. . 1 Design Department $2,400,000 10,000 12,000 i Variable . Assembly Department Variable $1,200,000 240,000 2,000 ' Assembly Department Fixed $2,400,000 Appended below are relevant data for three job. orders processed by R18 during December 20x8. Job Order #124 l #125 #126 Quantity in units 4,000 4,000 2,000 Direct Materials t $225,000 $232,000 * 40% assembled ** Normal Product Costs plus 30% Jobs #124 and #126 were completed within their respective specied deadlines and Job #125 is still in progress. Job #124 was delivered and billed in the last week of December 20x8. Accounting entries in the ledger account for Job #124 are as follows before MOH was posted in December 20x8: l Work in Process #124 I Direct Materials $225,000 ' Designer Fee $5,000 ' Assembly Labour $18,000 1 The balance, as at 30 November 20x8, in the MOH account was $9,250 Dr. In December 20x8, actual MOH incurred was $109,350 and applied MOH for the 3 jobs were yet to be recorded. Job #125 is an order for leather strap dress watches. The purchaser for raw material made an error on the leather straps ordered. The strap was 2 cm longer than required. When the error was discovered, production operators cut awaythe extra leather and discarded the extras as they could not be re-used. The additional leather costs 98 cents more per unit. The entire cost of leather straps was included in the material cost charged to the accounts. Wilson, a designer and account manager for Jobs #124 and #126 complained that the company's policy on overhead application cost him to earn less incentive payment for both jobs. He suggests that MOH should be applied using departmental rates based on appropriate cost drivers. With the help of other designers, he obtained the machine times used in the Design department for Jobs #124 and #126 were 40 hours and 50 hours respectively. In January 20x9, there was a phone call from the customer of Job #124 informing RJ'S that 50 units of watches were found to have broken glass faces. RlS has accepted responsibility for the return of the watches and the customer does not want replacements. Required: (a) Compute and record the necessary journal entries to account for the production costs and sales of Job #124 completed in the last week of December 20x8. (8 marks) (b) Based on information obtained in January 20x9 from the customer of Job #124, prepare necessary journal entries [0 record the costs related to the return of the 50 damaged units. Explain the impact on prots of Job #124 if the damaged units were treated as normal spoilage instead (show workings where relevant). (4 marks) (c) Compute the total amount of additional product costs that RIS will incur if, during 20248, the customer for Job #125 requested to increase the order from 4,000 to 5,000 units. State your assumptions where applicable. (1 1 marks) (d) (a) (1') (g) The designers' incentive payments are treated as period expenses Discuss the appropriateness of this accounting treatment in relation to determining product costs. (6 marks) Calculate the overfunder applied MOH for the year ended 31 December and write a journal entry to close this MOH variance. (4 marks) Explain the basis of Wilson's complaint with clear supporting computations. (8 marks) Using your knowledge of organisational architecture, explain if RIS should change the incentive scheme for designers. Give reasons to support your recommendation. (9 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts