Question: plz write neatly and circle u answer only answer to red!!! Don't just copy other Chegg answer!!! (1 point) An asset has value So =

plz write neatly and circle u answer only answer to red!!! Don't just copy other Chegg answer!!!

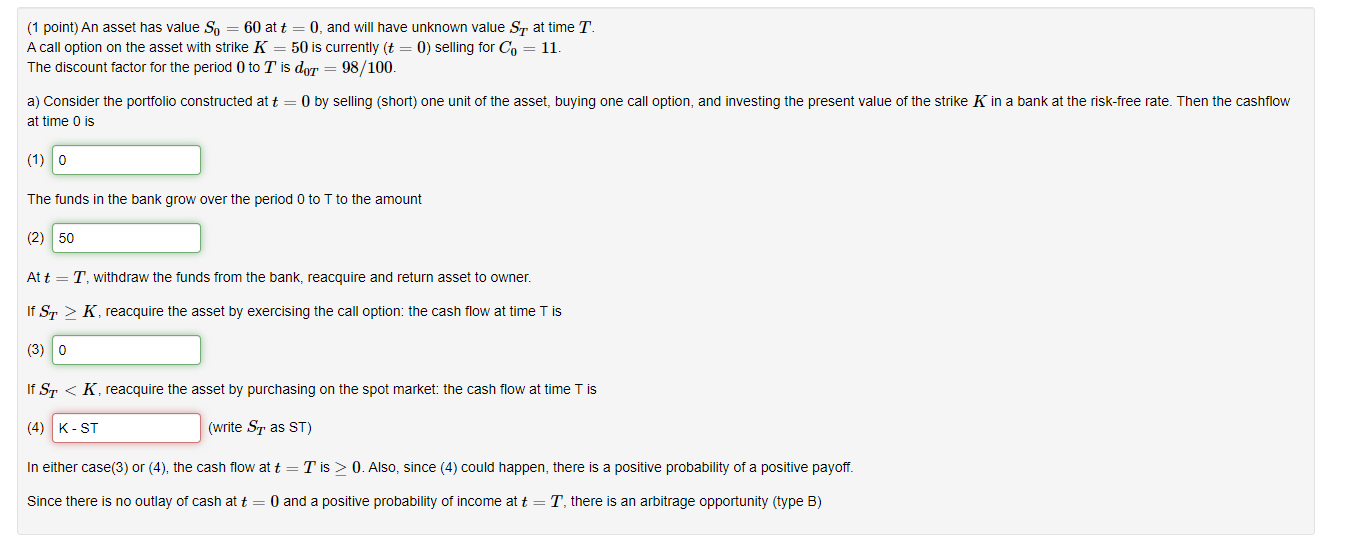

(1 point) An asset has value So = 60 at t=0, and will have unknown value St at time T. A call option on the asset with strike K 50 is currently (t = 0) selling for Co = 11. The discount factor for the period 0 to T is dor = 98/100. a) Consider the portfolio constructed at t = 0 by selling (short) one unit of the asset, buying one call option, and investing the present value of the strike K in a bank at the risk-free rate. Then the cashflow at time O is (1) O The funds in the bank grow over the period 0 to T to the amount (2) 50 At t =T, withdraw the funds from the bank, reacquire and return asset to owner. If ST > K, reacquire the asset by exercising the call option: the cash flow at time T is (3) 0 If St

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts