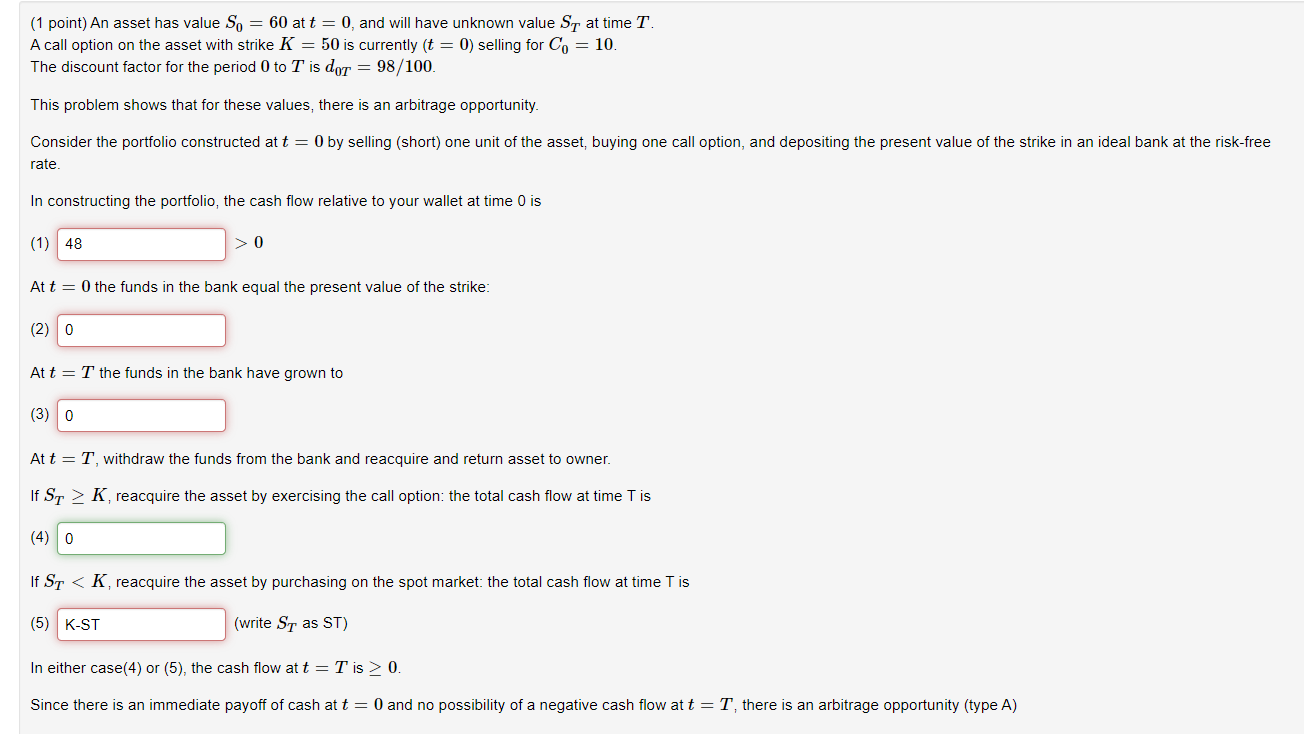

Question: plz write neatly and circle u answer only answer to red!!! Don't just copy Ch egg answer!!! (1 point)An asset has value SD = 60

plz write neatly and circle u answer

only answer to red!!!

Don't just copy Ch egg answer!!!

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock