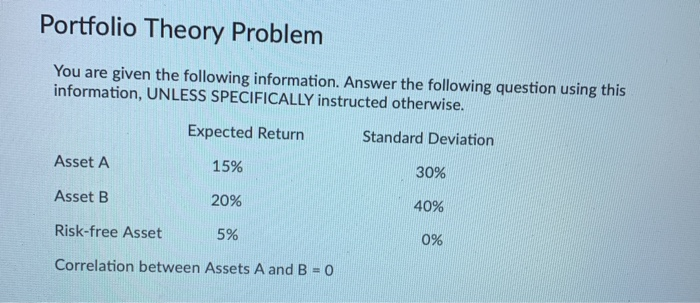

Question: Portfolio Theory Problem You are given the following information. Answer the following question using this information, UNLESS SPECIFICALLY instructed otherwise. Expected Return Standard Deviation Asset

Portfolio Theory Problem You are given the following information. Answer the following question using this information, UNLESS SPECIFICALLY instructed otherwise. Expected Return Standard Deviation Asset A 15% 30% Asset B 20% 40% Risk-free Asset 5% 0% Correlation between Assets A and B = 0 Question 12 (5 points) Assume you put 50% of your wealth in the risk-free asset and 50% into the minimum variance portfolio. On a new graph, show where you are in Expected Return/Standard deviation space

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock