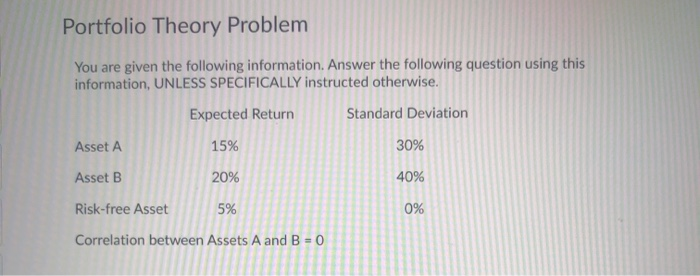

Question: Portfolio Theory Problem You are given the following information. Answer the following question using this information, UNLESS SPECIFICALLY instructed otherwise. Expected Return Standard Deviation Asset

Portfolio Theory Problem You are given the following information. Answer the following question using this information, UNLESS SPECIFICALLY instructed otherwise. Expected Return Standard Deviation Asset A 15% 30% Asset B 20% 40% Risk-free Asset 5% 0% Correlation between Assets A and B = 0 Question 11 (5 points) On your graph from the previous problem, circle the portfolios that are inefficient Why are they inefficient? A/ Question 12 (5 points) Assume you put 50% of your wealth in the risk-free asset and 50% into the minimum variance portfolio. On a new graph, show where you are in Expected Return/Standard deviation space. 5 Question 13 (5 points) What is the expected return and standard deviation of the portfolio you created in question 4? Is it an efficient portfolio? If you answered "no," show another portfolio on the graph that clearly dominates it in Expected Return/Standard Deviation space. Question 14 (5 points) Now assume that the correlation between Assets A and B is NEGATIVE 1 instead of 0. Does this present an arbitrage opportunity given all other expected returns and standard deviations are otherwise correct as given? For full credit, describe PRECISELY how you would engage in arbitrage. A/ Question 10 (5 points) In Expected Return/Standard Deviation space, graph the Investment Opportunity Set. You only need include Asset A, Asset B and the Minimum Variance/Standard Deviation portfolio in your graph, but make sure you show their expected returns and standard deviations labeled on the axes. A/

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts