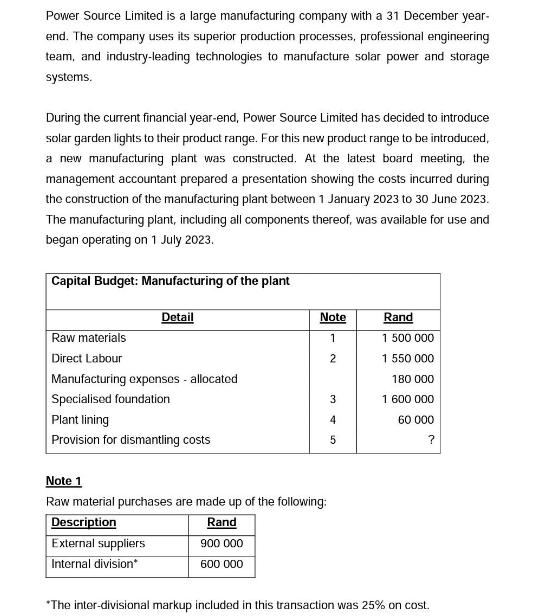

Power Source Limited is a large manufacturing company with a 31 December year- end. The company...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

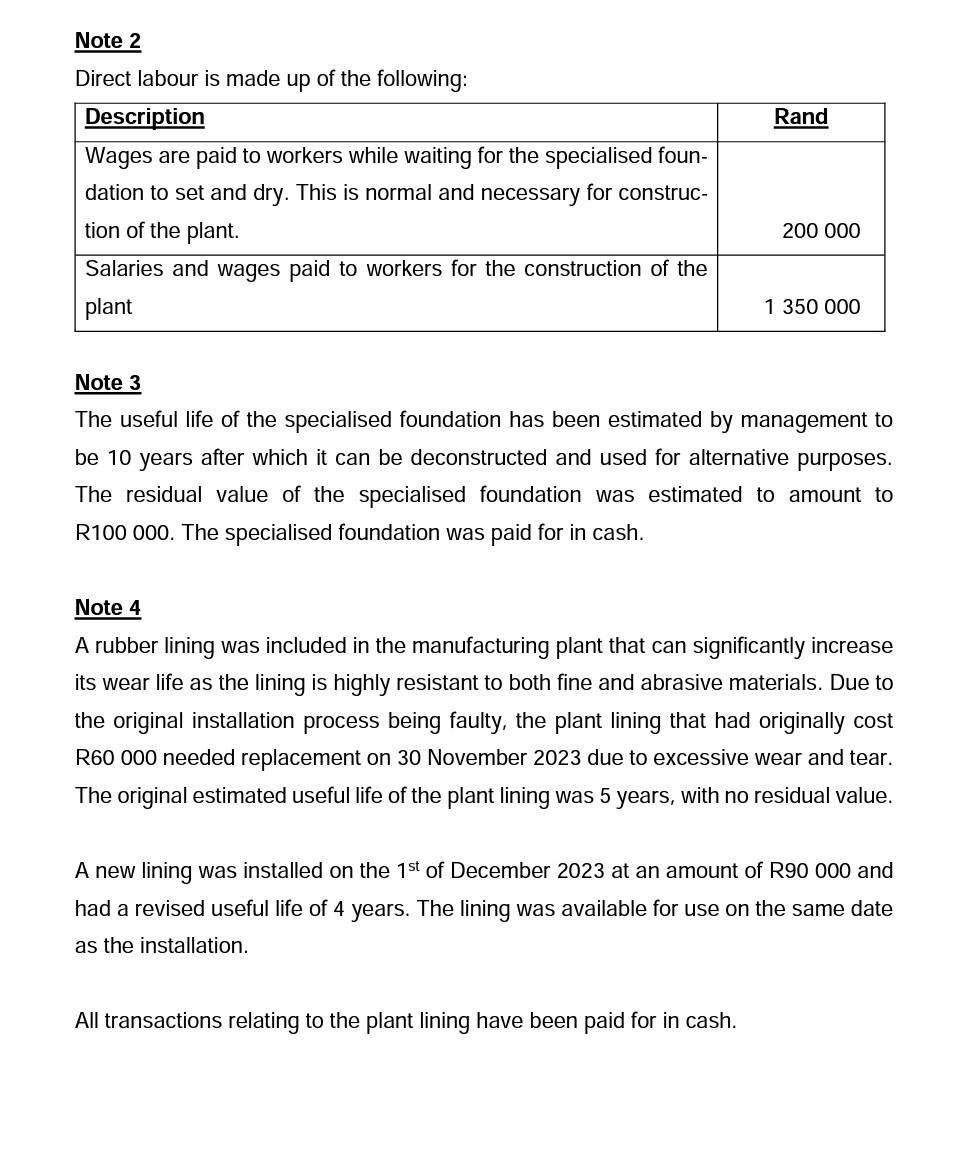

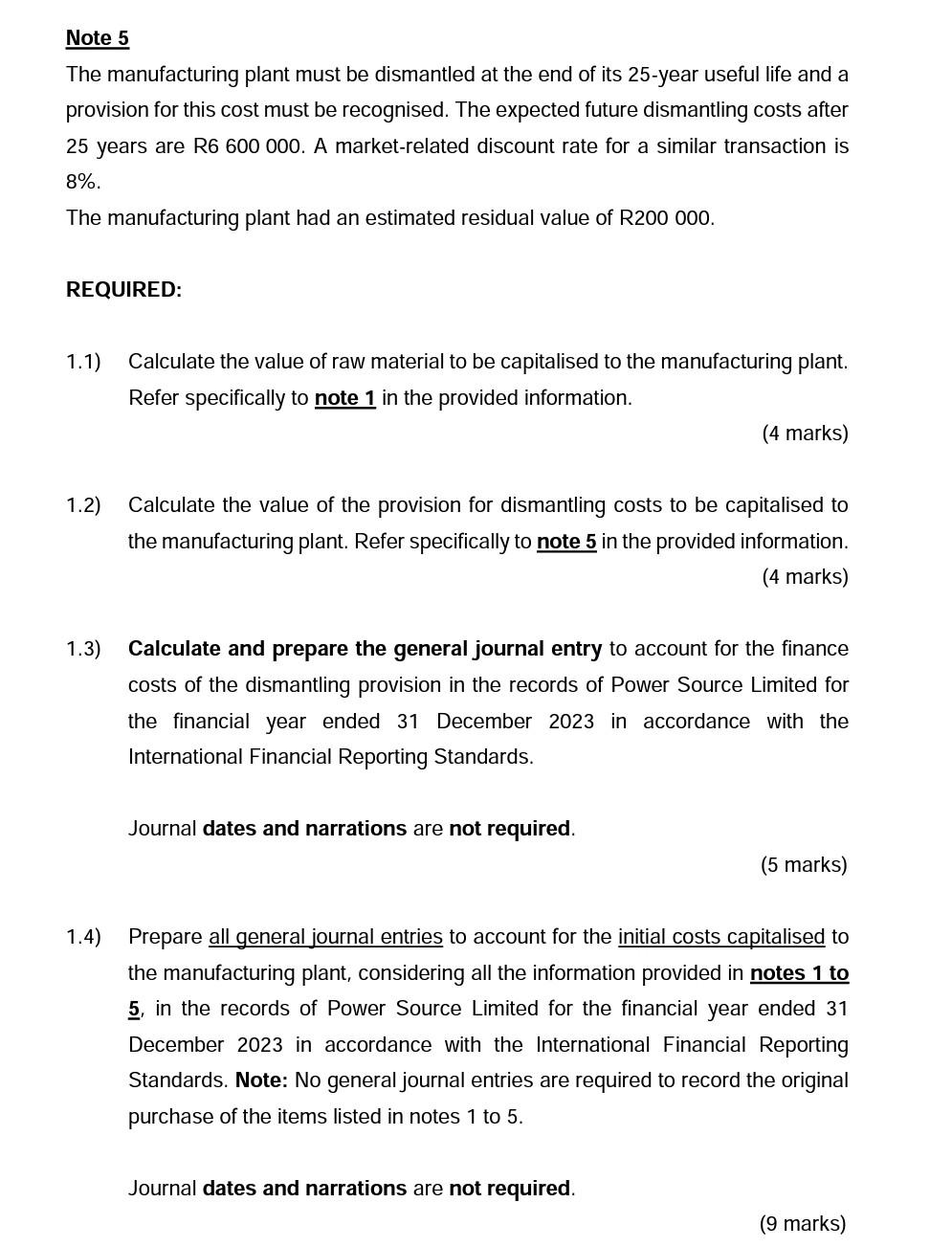

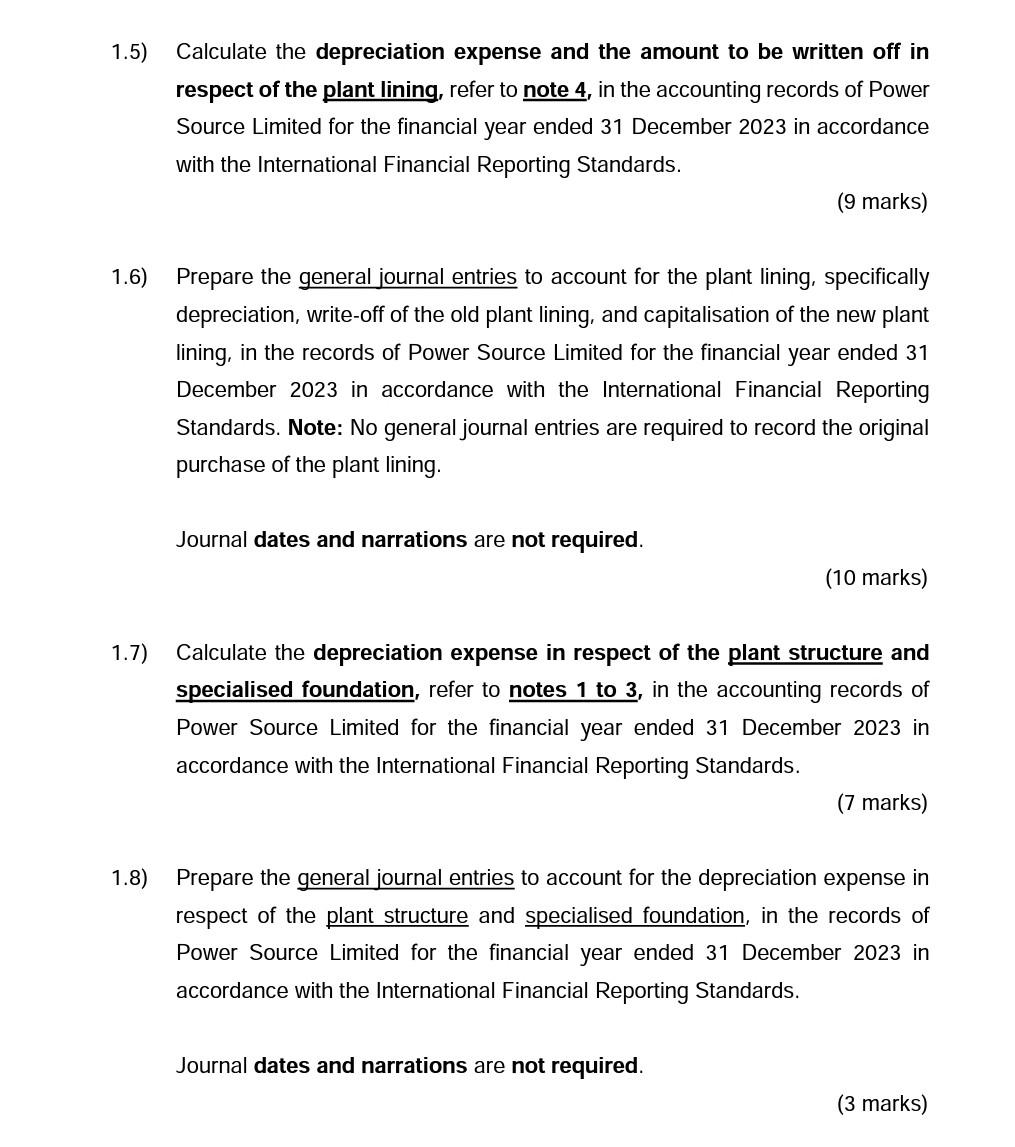

Power Source Limited is a large manufacturing company with a 31 December year- end. The company uses its superior production processes, professional engineering team, and industry-leading technologies to manufacture solar power and storage systems. During the current financial year-end, Power Source Limited has decided to introduce solar garden lights to their product range. For this new product range to be introduced, a new manufacturing plant was constructed. At the latest board meeting, the management accountant prepared a presentation showing the costs incurred during the construction of the manufacturing plant between 1 January 2023 to 30 June 2023. The manufacturing plant, including all components thereof, was available for use and began operating on 1 July 2023. Capital Budget: Manufacturing of the plant Raw materials Direct Labour Detail Manufacturing expensos - allocated Specialised foundation Plant lining Provision for dismantling costs Note 1 2 Note 1 Raw material purchases are made up of the following: Description Rand External suppliers Internal division* 900 000 600 000 3 4 5 Rand 1 500 000 1 550 000 180 000 1 600 000 60 000 ? *The inter-divisional markup included in this transaction was 25% on cost. Note 2 Direct labour is made up of the following: Description Wages are paid to workers while waiting for the specialised foun- dation to set and dry. This is normal and necessary for construc- tion of the plant. Salaries and wages paid to workers for the construction of the plant Rand 200 000 1 350 000 Note 3 The useful life of the specialised foundation has been estimated by management to be 10 years after which it can be deconstructed and used for alternative purposes. The residual value of the specialised foundation was estimated to amount to R100 000. The specialised foundation was paid for in cash. All transactions relating to the plant lining have been paid for in cash. Note 4 A rubber lining was included in the manufacturing plant that can significantly increase its wear life as the lining is highly resistant to both fine and abrasive materials. Due to the original installation process being faulty, the plant lining that had originally cost R60 000 needed replacement on 30 November 2023 due to excessive wear and tear. The original estimated useful life of the plant lining was 5 years, with no residual value. A new lining was installed on the 1st of December 2023 at an amount of R90 000 and had a revised useful life of 4 years. The lining was available for use on the same date as the installation. Note 5 The manufacturing plant must be dismantled at the end of its 25-year useful life and a provision for this cost must be recognised. The expected future dismantling costs after 25 years are R6 600 000. A market-related discount rate for a similar transaction is 8%. The manufacturing plant had an estimated residual value of R200 000. REQUIRED: 1.1) Calculate the value of raw material to be capitalised to the manufacturing plant. Refer specifically to note 1 in the provided information. 1.2) 1.3) Calculate the value of the provision for dismantling costs to be capitalised to the manufacturing plant. Refer specifically to note 5 in the provided information. (4 marks) (4 marks) Calculate and prepare the general journal entry to account for the finance costs of the dismantling provision in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Journal dates and narrations are not required. Journal dates and narrations are not required. (5 marks) 1.4) Prepare all general journal entries to account for the initial costs capitalised to the manufacturing plant, considering all the information provided in notes 1 to 5, in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Note: No general journal entries are required to record the original purchase of the items listed in notes 1 to 5. (9 marks) 1.5) Calculate the depreciation expense and the amount to be written off in respect of the plant lining, refer to note 4, in the accounting records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. 1.6) Prepare the general journal entries to account for the plant lining, specifically depreciation, write-off of the old plant lining, and capitalisation of the new plant lining, in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Note: No general journal entries are required to record the original purchase of the plant lining. 1.7) Journal dates and narrations are not required. (9 marks) (10 marks) Calculate the depreciation expense in respect of the plant structure and specialised foundation, refer to notes 1 to 3, in the accounting records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Journal dates and narrations are not required. (7 marks) 1.8) Prepare the general journal entries to account for the depreciation expense in respect of the plant structure and specialised foundation, in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. (3 marks) Power Source Limited is a large manufacturing company with a 31 December year- end. The company uses its superior production processes, professional engineering team, and industry-leading technologies to manufacture solar power and storage systems. During the current financial year-end, Power Source Limited has decided to introduce solar garden lights to their product range. For this new product range to be introduced, a new manufacturing plant was constructed. At the latest board meeting, the management accountant prepared a presentation showing the costs incurred during the construction of the manufacturing plant between 1 January 2023 to 30 June 2023. The manufacturing plant, including all components thereof, was available for use and began operating on 1 July 2023. Capital Budget: Manufacturing of the plant Raw materials Direct Labour Detail Manufacturing expensos - allocated Specialised foundation Plant lining Provision for dismantling costs Note 1 2 Note 1 Raw material purchases are made up of the following: Description Rand External suppliers Internal division* 900 000 600 000 3 4 5 Rand 1 500 000 1 550 000 180 000 1 600 000 60 000 ? *The inter-divisional markup included in this transaction was 25% on cost. Note 2 Direct labour is made up of the following: Description Wages are paid to workers while waiting for the specialised foun- dation to set and dry. This is normal and necessary for construc- tion of the plant. Salaries and wages paid to workers for the construction of the plant Rand 200 000 1 350 000 Note 3 The useful life of the specialised foundation has been estimated by management to be 10 years after which it can be deconstructed and used for alternative purposes. The residual value of the specialised foundation was estimated to amount to R100 000. The specialised foundation was paid for in cash. All transactions relating to the plant lining have been paid for in cash. Note 4 A rubber lining was included in the manufacturing plant that can significantly increase its wear life as the lining is highly resistant to both fine and abrasive materials. Due to the original installation process being faulty, the plant lining that had originally cost R60 000 needed replacement on 30 November 2023 due to excessive wear and tear. The original estimated useful life of the plant lining was 5 years, with no residual value. A new lining was installed on the 1st of December 2023 at an amount of R90 000 and had a revised useful life of 4 years. The lining was available for use on the same date as the installation. Note 5 The manufacturing plant must be dismantled at the end of its 25-year useful life and a provision for this cost must be recognised. The expected future dismantling costs after 25 years are R6 600 000. A market-related discount rate for a similar transaction is 8%. The manufacturing plant had an estimated residual value of R200 000. REQUIRED: 1.1) Calculate the value of raw material to be capitalised to the manufacturing plant. Refer specifically to note 1 in the provided information. 1.2) 1.3) Calculate the value of the provision for dismantling costs to be capitalised to the manufacturing plant. Refer specifically to note 5 in the provided information. (4 marks) (4 marks) Calculate and prepare the general journal entry to account for the finance costs of the dismantling provision in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Journal dates and narrations are not required. Journal dates and narrations are not required. (5 marks) 1.4) Prepare all general journal entries to account for the initial costs capitalised to the manufacturing plant, considering all the information provided in notes 1 to 5, in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Note: No general journal entries are required to record the original purchase of the items listed in notes 1 to 5. (9 marks) 1.5) Calculate the depreciation expense and the amount to be written off in respect of the plant lining, refer to note 4, in the accounting records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. 1.6) Prepare the general journal entries to account for the plant lining, specifically depreciation, write-off of the old plant lining, and capitalisation of the new plant lining, in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Note: No general journal entries are required to record the original purchase of the plant lining. 1.7) Journal dates and narrations are not required. (9 marks) (10 marks) Calculate the depreciation expense in respect of the plant structure and specialised foundation, refer to notes 1 to 3, in the accounting records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. Journal dates and narrations are not required. (7 marks) 1.8) Prepare the general journal entries to account for the depreciation expense in respect of the plant structure and specialised foundation, in the records of Power Source Limited for the financial year ended 31 December 2023 in accordance with the International Financial Reporting Standards. (3 marks)

Expert Answer:

Answer rating: 100% (QA)

Lets go through each of the requirements step by step 11 Calculate the value of raw material ... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

What is a lump-sum settlement? What kind of beneficiary would benefit the most from this option? What is an installment payments settlement? When would an insured individual choose this option? What...

-

The following are independent situations for which you will recommend an appropriate audit report: 1. Subsequent to the date of the financial statements as part of his post-financial report date...

-

The following are independent situations for which you will recommend an appropriate audit report: 1. Subsequent to the date of the financial statements as part of his post-balance sheet date audit...

-

Adel runs a construction equipment rental company, renting out loaders, generators, lifts and similar equipment on short term rentals. In the past, Adel has purchased the equipment he then rents out,...

-

Boyles Law states that when a sample of gas is compressed at a constant temperature, the pressure P and volume V satisfy the equation PV = C, where C is a constant. Suppose that at a certain instant...

-

Find the product. (6+7x)2

-

Suppose \(F(S, t)\) is the forward price of a commodity with no storage cost and governed by \(\mathrm{d} S(t)=\mu \mathrm{d} t+\sigma \mathrm{d} z\) and terminating at time \(T\). What is the...

-

How much and in which ways did unbridled self-interest contribute to the subprime lending crisis?

-

How is this programmed in C. Image transcription text Mobile robots are commonly used to transport objects ?'om a start position to a goal position (e.g.= warehouse}. This can be achieved by line...

-

According to the assigned case study, Lawn King must develop an S&OP plan that considers the costs of inventory, overtime, hiring, and layoff (beware of stock outs). If the plan results in back...

-

There are three customer locations with x- and y-coordinates of (0, 0), (4, 3), and (1, 1), respectively. The projected shipment volumes are 12, 20, and 18, respectively. Using the center-of-gravity...

-

Standard economic theory is based on the assumption that people behave rationally. The winners curse implies that people behave irrationally by paying more for an asset than it is worth. Can we...

-

How much should you eat at an all-you-can-eat restaurant?

-

Write down the equipment-independent and equipment-dependent relationships for a distillation column.

-

Consider the following statement: "The Solow model shows that the saving rate does not affect the growth rate in the long run, so we should stop worrying about the low US saving rate. Increasing the...

-

Suppose the government amends the constitution to prevent government officials from negotiating with terrorists. What are the advantages of such a policy? What are the disadvantages?

-

A nichrome wire is 1m long and 1x10 -6 m 2 incross-sectional area. When connected to a potential difference of2V, a current of 4A exists in the wire. The resistivity of thisnichrome is? i pretty sure...

-

Wimot Trucking Corporation uses the units-of-production depreciation method because units-of-production best measures wear and tear on the trucks. Consider these facts about one Mack truck in the...

-

Exhibit 14.10 presents data on market-to-book (MB) ratios, ROCE, the cost of equity capital, and price-earnings (PE) ratios for seven pharmaceutical companies. (Note that PE ratios for these firms...

-

The chapter demonstrates how to prepare a statement of cash flows from information on the balance sheet and income statement. If this is possible, why are managers required to provide a statement of...

-

Exhibit 5.24 presents balance sheets for Year 2 and Year 3 for Whole Foods Market, Inc.; Exhibit 5.25 presents income statements for Year 1 through Year 3. REQUIRED a. For Year 3, prepare the...

-

An \(80 \mathrm{~kg}\) man standing on a frozen lake tosses a 0. 500 \(\mathrm{kg}\) football to his dog. (a) If the ball leaves his hands at \(15 \mathrm{~m} / \mathrm{s}\) relative to Earth, what...

-

A small block of wood of inertia \(m_{\text {block }}\) is released from rest a distance \(b\) above the ground, directly above your head. You decide to shoot it with your pellet gun, which fires a...

-

Draw before and after energy bars for the collision shown in Figure \(6.8 a\) and \(6.8 b\). Data from Figure 6.8 (a) Earth reference frame (b) Reference frame M (DEM == 0.20 m/s) = 0 FM2 ME NIZ E...

Study smarter with the SolutionInn App