Prius Enterprises, a publicly traded company, is considering acquiring Juniper Inc, a private company in the same

Question:

Prius Enterprises, a publicly traded company, is considering acquiring Juniper Inc, a private company in the same business. Assume that both Prius and Juniper are stable growth companies funded entirely with equity, each with expected free cash flows next year of $ 10 million, and each expected to grow 4% a year in perpetuity The unlevered beta for the sector is 0.80 but only 40% of the risk in the business is market risk. The riskfree rate is 5% and the equity risk premium is 4%. (Tax rate = 40% for both firms).

a. Prius Enterprises has 5 million shares outstanding. Estimate the value per share for Prius as a stand-alone firm.

b. Estimate the value of Juniper as a stand-alone firm to its existing owner (who is not diversified).

c. Assume that Prius pays a premium of 50% over the estimated value of Juniper (from part b). Estimate the value per share of Prius after the transaction.

d. Now assume that Prius will be able to write up the book value of Juniper’s assets from the existing value of $ 100 million to $ 150 million. Assuming that these assets have five years of depreciable life left and that you use straight line depreciation, estimate the value of the additional tax savings that will accrue from the transaction.

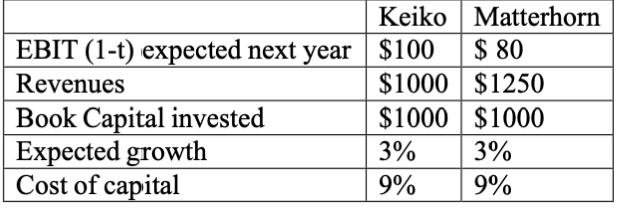

2. Keiko Inc., an entertainment company, is considering an acquisition of Matterhorn Inc., a maker of animated movies. The information on the two companies is provided below ($ values are in millions):

a. Estimate the value of the combined company, assuming no synergy in the merger.

b. Now assume that Keiko Inc. believes that the combined company will be much stronger, relative to the competition, and will therefore be able to find more new investments in the next 4 years (doubling the reinvestment rate over that period for the combined firm) and earn a return on capital of 12% on new investments in perpetuity. (Existing investments at both firms will continue to generate their existing returns on capital) After year 4, the growth rate will drop back to 3% but the return on capital will stay at 12%. Estimate the value of synergy in this merger.

Expert Answer:

Here are the steps and calculations for the questions 1a Value per share for Prius as a standalone firm Expected FCFF next year 10 million Growth rate ... View the full answer

Foundations of Financial Management

ISBN: 978-1259024979

10th Canadian edition

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta