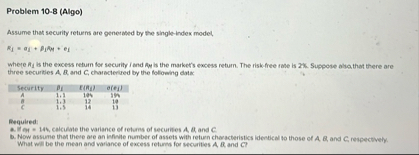

Question: Problem 1 0 - 8 ( Algo ) Assume that security returns are generafed by the single - index model, R I = I I

Problem Algo

Assume that security returns are generafed by the singleindex model,

three securties and characterired by the following data

tableSecurityEheeiA

enquired:

a er calculate the variance of rehams of securiles and

b Now assume that these are an inhilie number of assets with return chawacteristics idevical to those of A R and C respectivety, What will be the mean and warlance of excess returms for lecorities A A and

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock