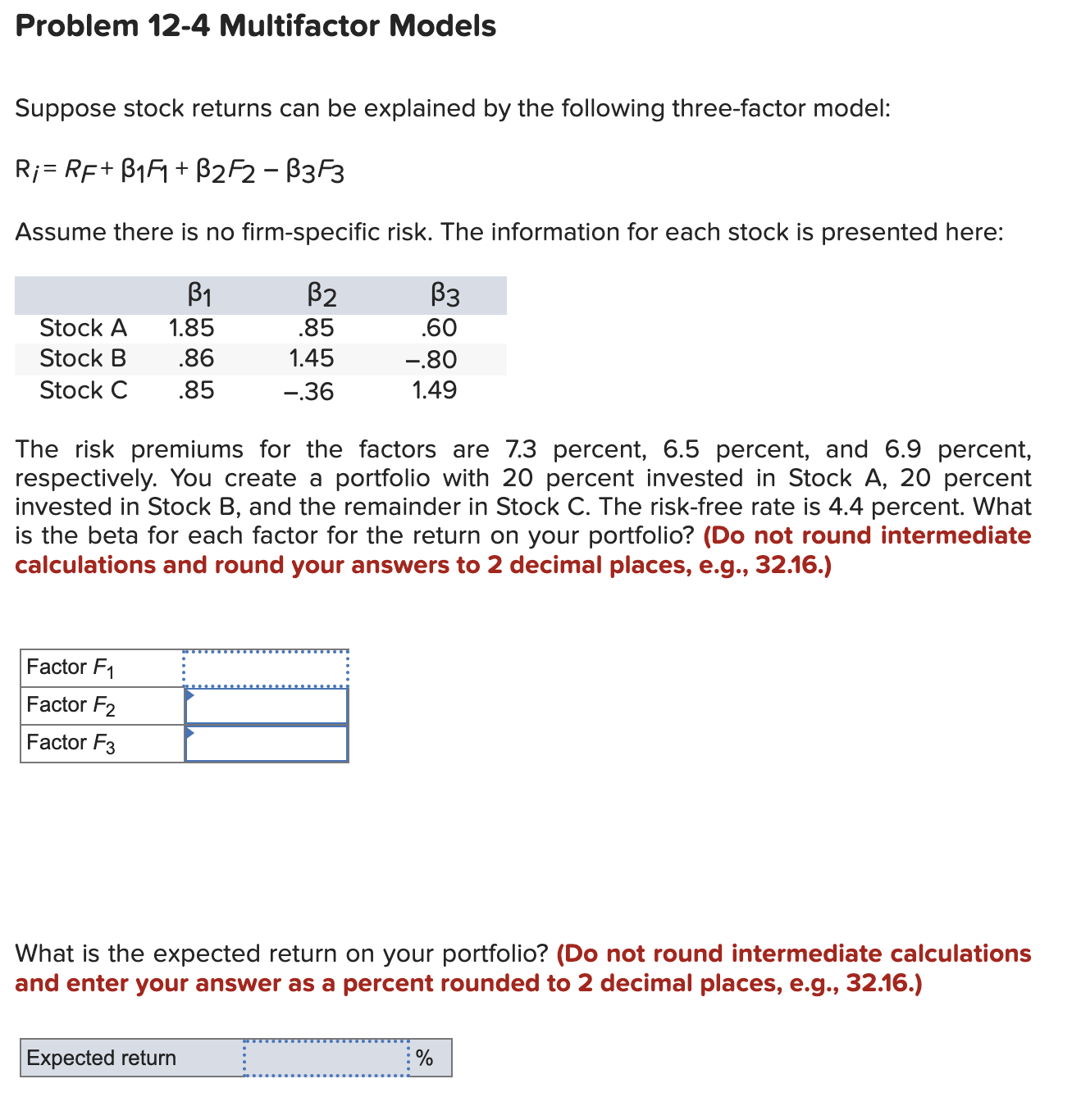

Question: Problem 1 2 - 4 Multifactor Models Suppose stock returns can be explained by the following three - factor model: R i = R F

Problem Multifactor Models

Suppose stock returns can be explained by the following threefactor model:

Assume there is no firmspecific risk. The information for each stock is presented here:

The risk premiums for the factors are percent, percent, and percent,

respectively. You create a portfolio with percent invested in Stock A percent

invested in Stock B and the remainder in Stock C The riskfree rate is percent. What

is the beta for each factor for the return on your portfolio? Do not round intermediate

calculations and round your answers to decimal places, eg

What is the expected return on your portfolio? Do not round intermediate calculations

and enter your answer as a percent rounded to decimal places, eg

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock