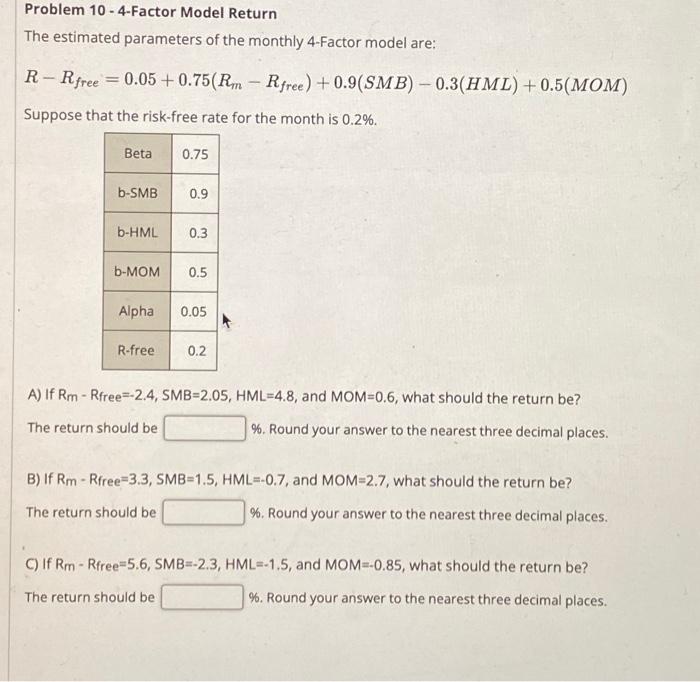

Question: Problem 10-4-Factor Model Return The estimated parameters of the monthly 4-Factor model are: R-R free = 0.05 +0.75(Rm - Rfree) +0.9(SMB) 0.3(HML) +0.5(MOM) Suppose that

Problem 10 - 4-Factor Model Return The estimated parameters of the monthly 4-Factor model are: RRfree=0.05+0.75(RmRfree)+0.9(SMB)0.3(HML)+0.5(MOM) Suppose that the risk-free rate for the month is 0.2%. A) If Rm - Rfree=2.4,SMB=2.05,HML=4.8, and MOM=0.6, what should the return be? The return should be \%. Round your answer to the nearest three decimal places. B) If RmRfree=3.3,SMB=1.5,HML=0.7, and MOM=2.7, what should the return be? The return should be \%. Round your answer to the nearest three decimal places. C) If RmRfree=5.6,SMB=2.3,HML=1.5, and MOM=0.85, what should the return be? The return should be \%. Round your answer to the nearest three decimal places

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts