Question: Problem 2 (10 points) Suppose Arbitrage Pricing Theory is valid in a simple market. Assume the excess return on portfolio i follows single factor model

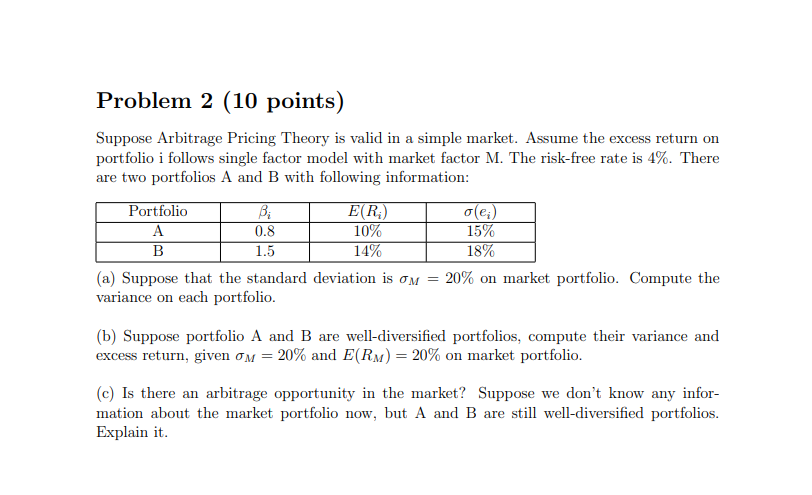

Problem 2 (10 points) Suppose Arbitrage Pricing Theory is valid in a simple market. Assume the excess return on portfolio i follows single factor model with market factor M. The risk-free rate is 4%. There are two portfolios A and B with following information: Portfolio Bi E(R) ole:) A 0.8 10% 15% B 14% 18% (a) Suppose that the standard deviation is om = 20% on market portfolio. Compute the variance on each portfolio. 1.5 (b) Suppose portfolio A and B are well-diversified portfolios, compute their variance and excess return, given om = 20% and E(RM) = 20% on market portfolio. (c) Is there an arbitrage opportunity in the market? Suppose we don't know any infor- mation about the market portfolio now, but A and B are still well-diversified portfolios. Explain it

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts