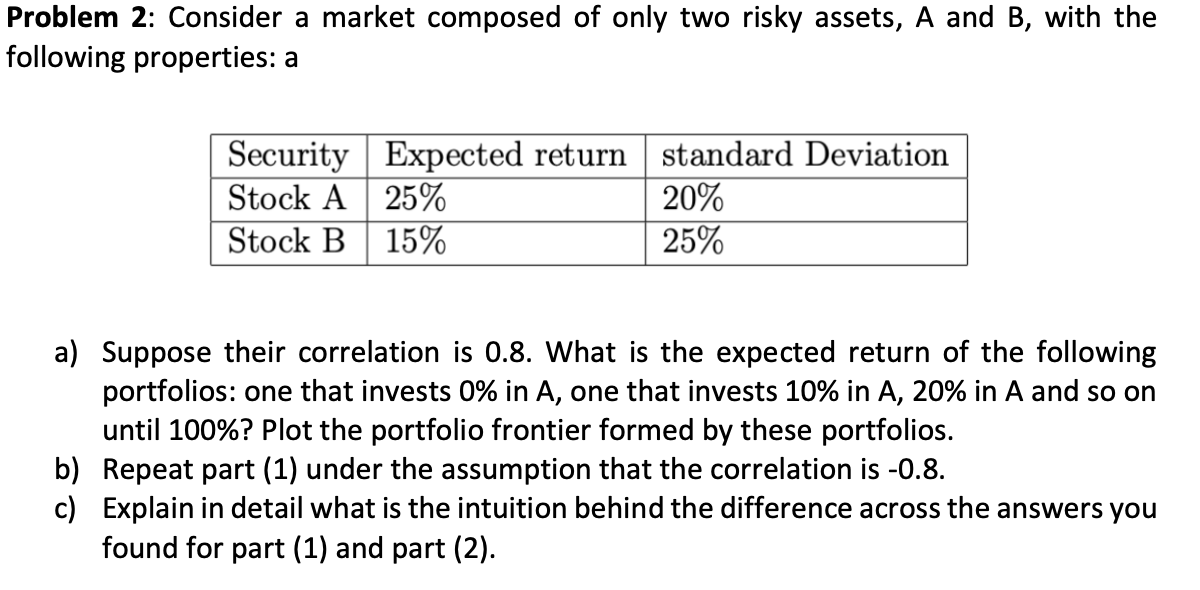

Question: Problem 2: Consider a market composed of only two risky assets, A and B, with the following properties: a | Security | Stock A Stock

Problem 2: Consider a market composed of only two risky assets, A and B, with the following properties: a | Security | Stock A Stock B Expected return 25% 15% standard Deviation 20% 25% a) Suppose their correlation is 0.8. What is the expected return of the following portfolios: one that invests 0% in A, one that invests 10% in A, 20% in A and so on until 100%? Plot the portfolio frontier formed by these portfolios. b) Repeat part (1) under the assumption that the correlation is -0.8. c) Explain in detail what is the intuition behind the difference across the answers you found for part (1) and part (2). Problem 2: Consider a market composed of only two risky assets, A and B, with the following properties: a | Security | Stock A Stock B Expected return 25% 15% standard Deviation 20% 25% a) Suppose their correlation is 0.8. What is the expected return of the following portfolios: one that invests 0% in A, one that invests 10% in A, 20% in A and so on until 100%? Plot the portfolio frontier formed by these portfolios. b) Repeat part (1) under the assumption that the correlation is -0.8. c) Explain in detail what is the intuition behind the difference across the answers you found for part (1) and part (2)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts