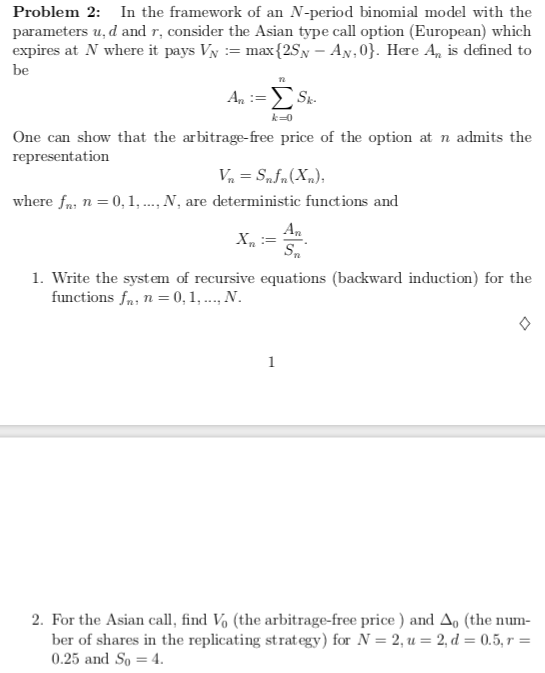

Question: Problem 2: In the framework of an N-period binomial model with the parameters u, d and r, consider the Asian type call option (European) which

Problem 2: In the framework of an N-period binomial model with the parameters u, d and r, consider the Asian type call option (European) which expires at N where it pays Vy := max {2S - An,0}. Here A, is defined to be An s. k=0 One can show that the arbitrage-free price of the option at n admits the representation Vn=Shfn(x), where fnn=0,1,..., N, are deterministic functions and X= Sn 1. Write the system of recursive equations (backward induction) for the functions fn, n=0,1,..., N. 2. For the Asian call, find V. (the arbitrage-free price ) and A, (the num- ber of shares in the replicating strategy) for N = 2, u = 2, d = 0.5, r = 0.25 and So = 4. Problem 2: In the framework of an N-period binomial model with the parameters u, d and r, consider the Asian type call option (European) which expires at N where it pays Vy := max {2S - An,0}. Here A, is defined to be An s. k=0 One can show that the arbitrage-free price of the option at n admits the representation Vn=Shfn(x), where fnn=0,1,..., N, are deterministic functions and X= Sn 1. Write the system of recursive equations (backward induction) for the functions fn, n=0,1,..., N. 2. For the Asian call, find V. (the arbitrage-free price ) and A, (the num- ber of shares in the replicating strategy) for N = 2, u = 2, d = 0.5, r = 0.25 and So = 4

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts