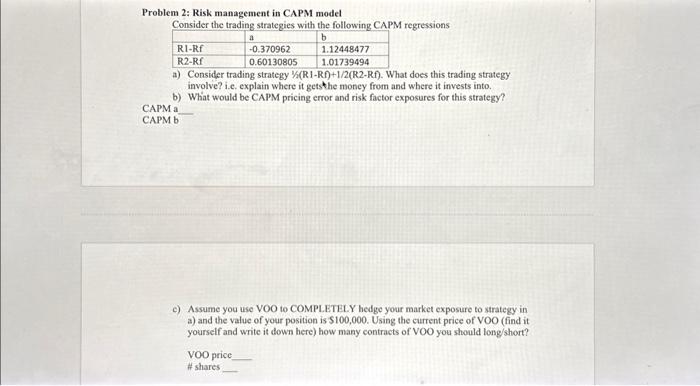

Question: Problem 2: Risk management in CAPM model Consider the tradine stratesies with the followine CAPM regressions a) Consider trading strategy 1//(R1Rf)+1/2 (R2-Rf). What does this

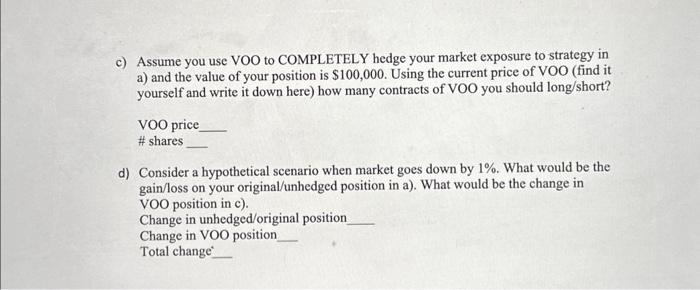

Problem 2: Risk management in CAPM model Consider the tradine stratesies with the followine CAPM regressions a) Consider trading strategy 1//(R1Rf)+1/2 (R2-Rf). What does this trading strategy involve? i.c. explain where it getsthe money from and where it invests into. b) What would be CAPM pricing error and risk factor exposures for this strategy? CAPMa CAPM b e) Assume you use VOO to COMPLETHLY hedge your market exposure to strategy in a) and the value of your position is $100,000. Using the current price of VOO (find it yourself and write it down here) how many contracts of voO you should tong/short? voO price \# shares c) Assume you use VOO to COMPLETELY hedge your market exposure to strategy in a) and the value of your position is $100,000. Using the current price of VOO (find it yourself and write it down here) how many contracts of VOO you should long/short? VOO price \# shares d) Consider a hypothetical scenario when market goes down by 1%. What would be the gain/loss on your original/unhedged position in a). What would be the change in VOO position in c). Change in unhedged/original position Change in VOO position Total change*

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts