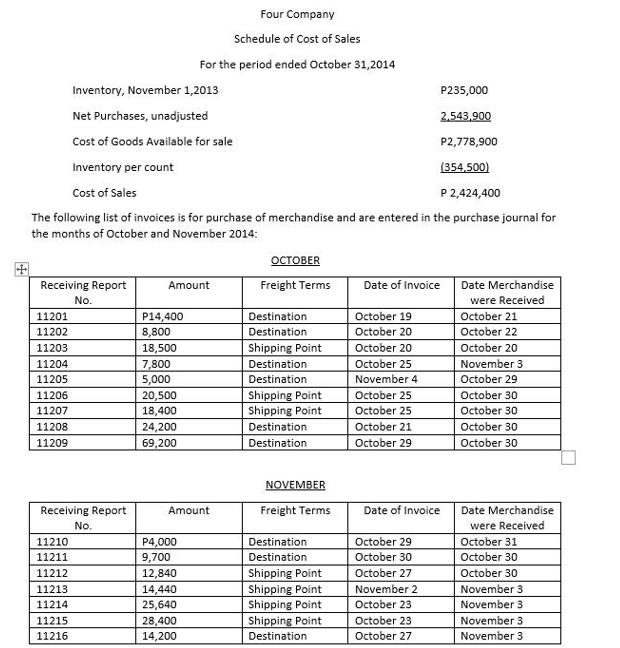

1. The adjusted balance of the inventory account as of October 31, 2014? 2. The correct cost...

Fantastic news! We've Found the answer you've been seeking!

Question:

1. The adjusted balance of the inventory account as of October 31, 2014?

2. The correct cost of sales for the period ended October 31, 2014?

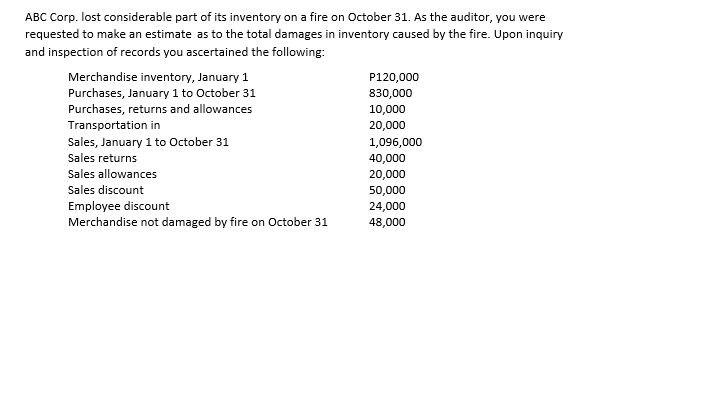

1. Using the gross profit test, what was the estimated loss in inventory due to the fire assuming that the gross profit rate is 30% based on sales?

2. Using the gross profit test, what was the estimated loss in inventory due to the fire assuming that the gross profit rate is 25% based on cost?

Expert Answer:

To determine the estimated loss in inventory due to the fire using the gross profit test we need to calculate the cost of goods sold and then estimate the inventory loss based on the given gross profi... View the full answer

Related Book For

College Accounting A Contemporary Approach

ISBN: 978-0077639730

3rd edition

Authors: David Haddock, John Price, Michael Farina

Posted Date: