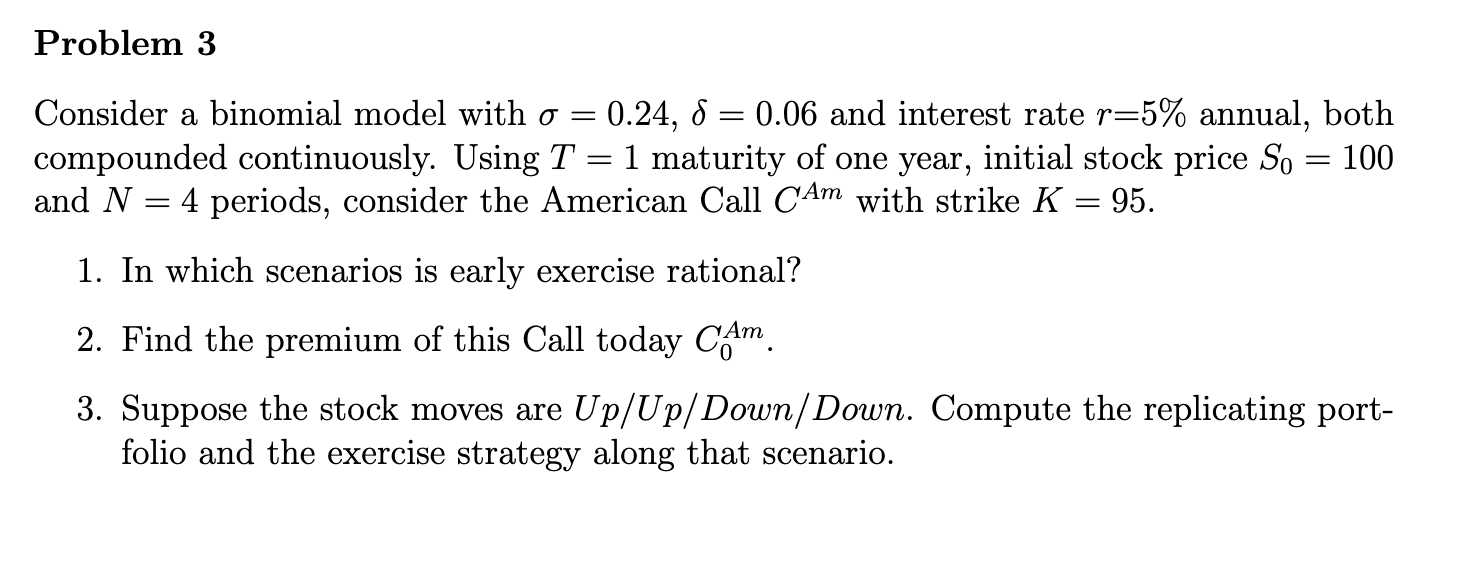

Question: Problem 3 Consider a binomial model with = 0 . 2 4 , = 0 . 0 6 and interest rate r = 5 %

Problem

Consider a binomial model with and interest rate annual, both

compounded continuously. Using maturity of one year, initial stock price

and periods, consider the American Call with strike

In which scenarios is early exercise rational?

Find the premium of this Call today

Suppose the stock moves are own. Compute the replicating port

folio and the exercise strategy along that scenario.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock