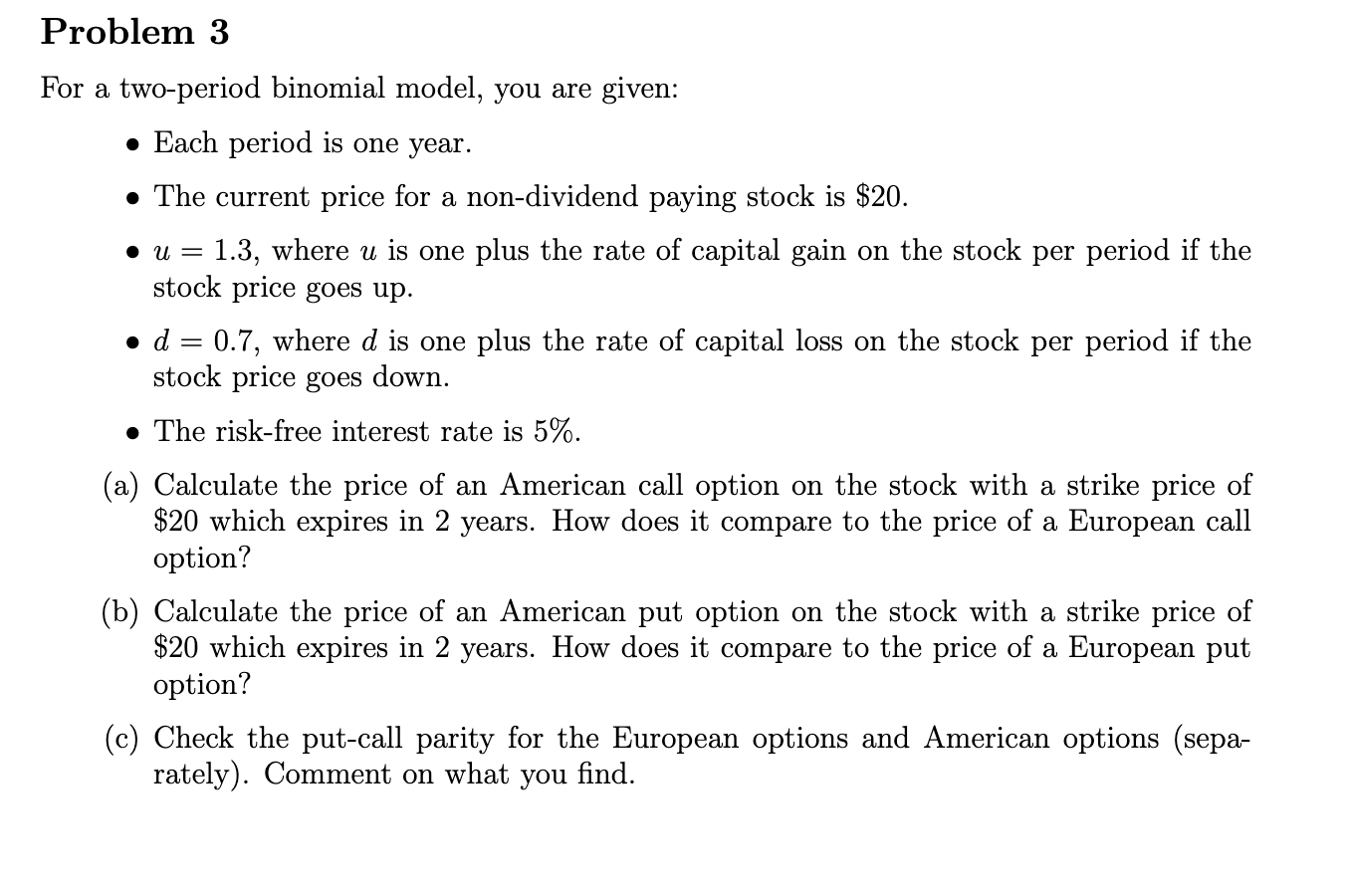

Question: Problem 3 For a two - period binomial model, you are given: Each period is one year. The current price for a non - dividend

Problem

For a twoperiod binomial model, you are given:

Each period is one year.

The current price for a nondividend paying stock is $

where is one plus the rate of capital gain on the stock per period if the

stock price goes up

where is one plus the rate of capital loss on the stock period if the

stock price goes down.

The riskfree interest rate is

a Calculate the price of an American call option on the stock with a strike price of

$ which expires in years. How does it compare to the price of a European call

option?

b Calculate the price of an American put option on the stock with a strike price of

$ which expires in years. How does it compare to the price of a European put

option?

c Check the putcall parity for the European options and American options sepa

rately Comment on what you find.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock