Question: Problem 4. (25 points) Consider a two-period market with a bond B and an asset S. The periodic interest rate is assumed to be r

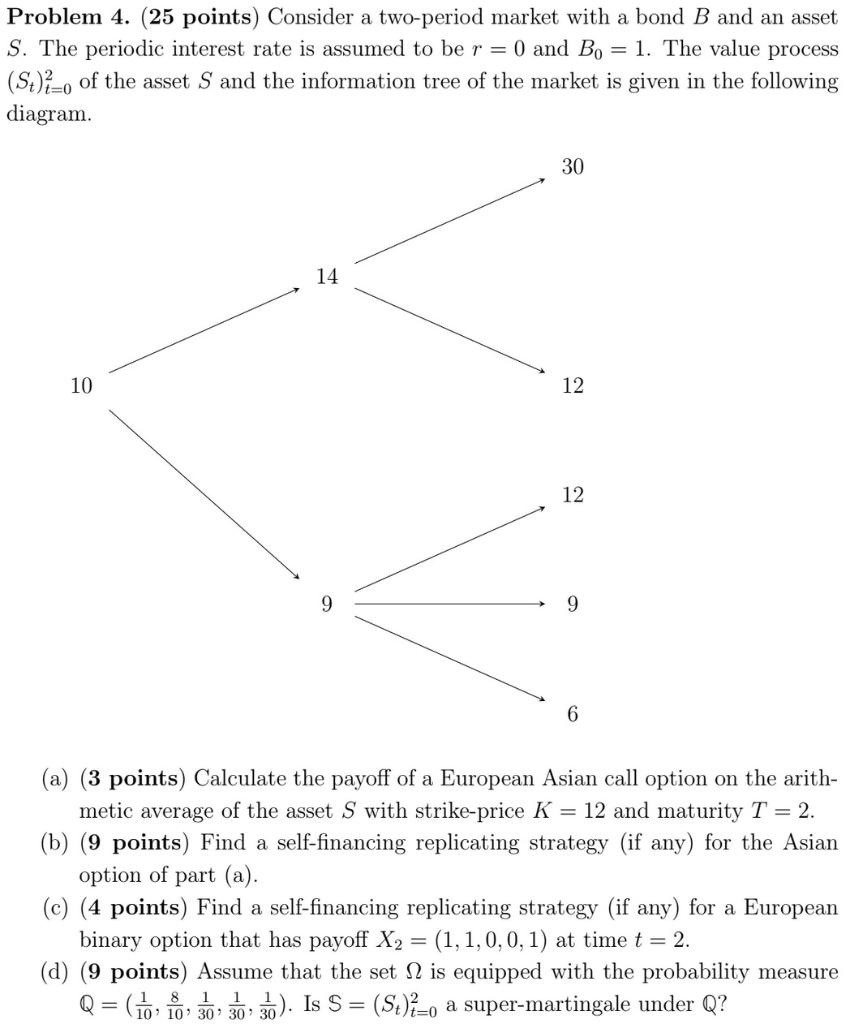

Problem 4. (25 points) Consider a two-period market with a bond B and an asset S. The periodic interest rate is assumed to be r = 0 and Bo = 1. The value process (St);o of the asset S and the information tree of the market is given in the following diagram. 30 14 10 12 12 9 9 6 (a) (3 points) Calculate the payoff of a European Asian call option on the arith- metic average of the asset S with strike-price K = 12 and maturity T = 2. (b) (9 points) Find a self-financing replicating strategy (if any) for the Asian option of part (a). (c) (4 points) Find a self-financing replicating strategy (if any) for a European binary option that has payoff X2 = (1,1,0,0,1) at time t = 2. (d) (9 points) Assume that the set 12 is equipped with the probability measure Q = Go to, 30; 30; 3o). Is S = (St){=o a super-martingale under Q? 1 10 Problem 4. (25 points) Consider a two-period market with a bond B and an asset S. The periodic interest rate is assumed to be r = 0 and Bo = 1. The value process (St);o of the asset S and the information tree of the market is given in the following diagram. 30 14 10 12 12 9 9 6 (a) (3 points) Calculate the payoff of a European Asian call option on the arith- metic average of the asset S with strike-price K = 12 and maturity T = 2. (b) (9 points) Find a self-financing replicating strategy (if any) for the Asian option of part (a). (c) (4 points) Find a self-financing replicating strategy (if any) for a European binary option that has payoff X2 = (1,1,0,0,1) at time t = 2. (d) (9 points) Assume that the set 12 is equipped with the probability measure Q = Go to, 30; 30; 3o). Is S = (St){=o a super-martingale under Q? 1 10

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts