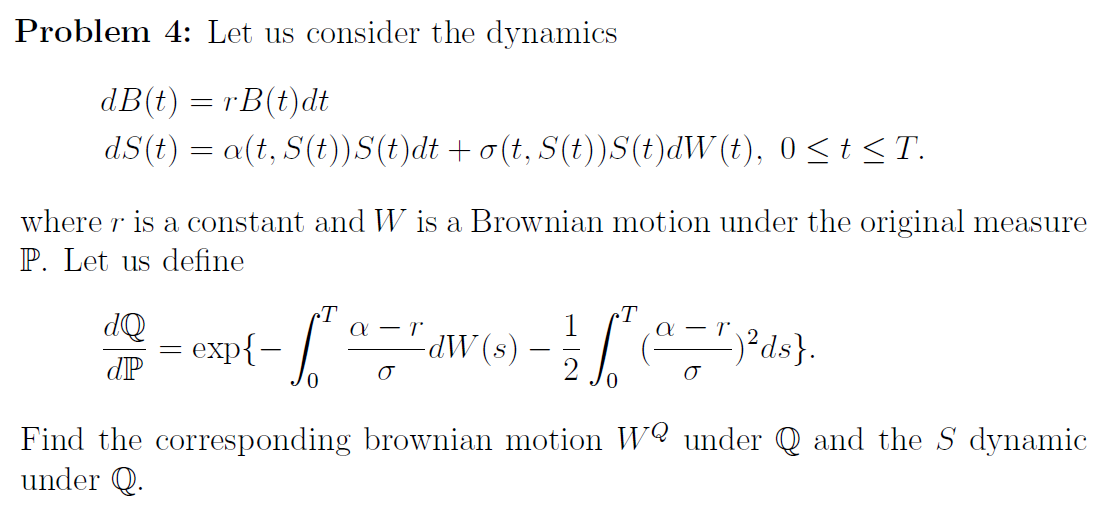

Question: Problem 4: Let us consider the dynamics dB(t)=rB(t)dtdS(t)=(t,S(t))S(t)dt+(t,S(t))S(t)dW(t),0tT where r is a constant and W is a Brownian motion under the original measure P. Let

Problem 4: Let us consider the dynamics dB(t)=rB(t)dtdS(t)=(t,S(t))S(t)dt+(t,S(t))S(t)dW(t),0tT where r is a constant and W is a Brownian motion under the original measure P. Let us define dPdQ=exp{0TrdW(s)210T(r)2ds}. Find the corresponding brownian motion WQ under Q and the S dynamic under

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock