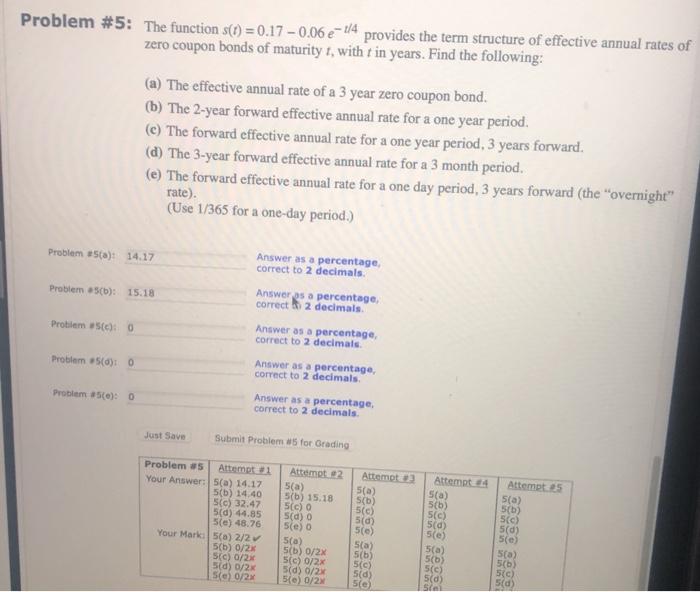

Question: Problem #5: The function s(t) = 0.17 -0.06 - 1/4 provides the term structure of effective annual rates of zero coupon bonds of maturity 1,

Problem #5: The function s(t) = 0.17 -0.06 - 1/4 provides the term structure of effective annual rates of zero coupon bonds of maturity 1, with tin years. Find the following: (a) The effective annual rate of a 3 year zero coupon bond. (b) The 2-year forward effective annual rate for a one year period. (e) The forward effective annual rate for a one year period, 3 years forward. (d) The 3-year forward effective annual rate for a 3 month period. (e) The forward effective annual rate for a one day period, 3 years forward (the "overnight" rate). (Use 1/365 for a one-day period.) Problem Sta) 14.17 Answer as a percentage, correct to 2 decimals. Problema 5cb): 15.18 Answer as a percentage correct 2 decimals Problem (c): 0 Answer as a percentage, correct to 2 decimals Problem 5(d): 0 Answer as a percentage, correct to 2 decimals Probleme): 0 Answer as a percentage, correct to 2 decimals Just Save Submit Problem for Grading Attempt s(a) 5(b) Problems Attempt 1 Your Answer: 5(a) 14.17 5(b) 14.40 (c) 32.47 5(d) 44.85 Sle) 48.76 Your Mark 5(a) 2/2 5(b) 0/2 Sic) 0/2 (d) 0/2 se 0/2 5(0) Attempt 2 5(a) 5(b) 15.18 5(c) 5(d) 5(e) 5(a) 5(b) 0/2 5(c) 0/2 5(d) 0/2 50) 0/2 5(0) Attempt 5(a) 5(b) 5(c) 5(0) 5(e) Sca) 5(b) 5(0) 5(0) 5(e) 5(e) 5(a) 5(b) 5(e) 5(d) Attempt as (a 5(b) 5(0) 5(d) 5(e) Sca) 5(b) 5(0) 5(d) Sie

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts