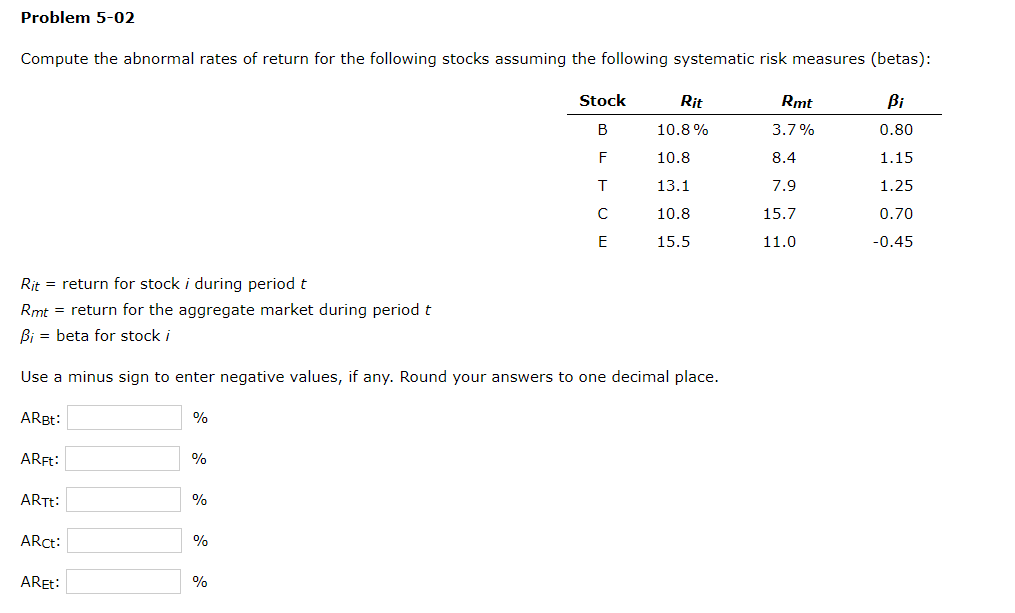

Question: Problem 5-02 Compute the abnormal rates of return for the following stocks assuming the following systematic risk measures (betas): Stock - Rmt 0.80 1.15 Rit

Problem 5-02 Compute the abnormal rates of return for the following stocks assuming the following systematic risk measures (betas): Stock - Rmt 0.80 1.15 Rit 10.8% 10.8 13.1 10.8 15.5 3.7% 8.4 7.9 15.7 11.0 1.25 0.70 -0.45 E Rit = return for stock i during period t Rmt = return for the aggregate market during period t Bi = beta for stock i Use a minus sign to enter negative values, if any. Round your answers to one decimal place. ARBE: ARFt: ARTt: Arct: ARE

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock