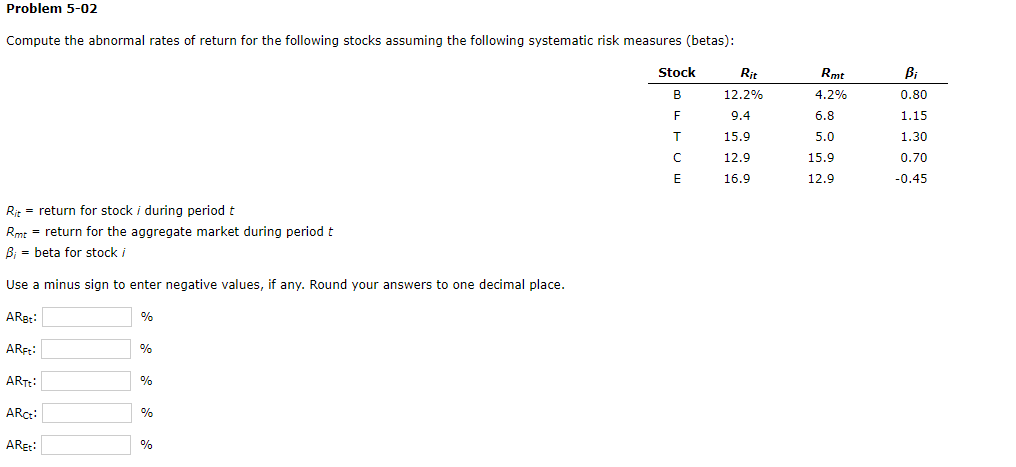

Question: Problem 5-02 Compute the abnormal rates of return for the following stocks assuming the following systematic risk measures (betas): Stock B F Rmt 4.2% 6.8

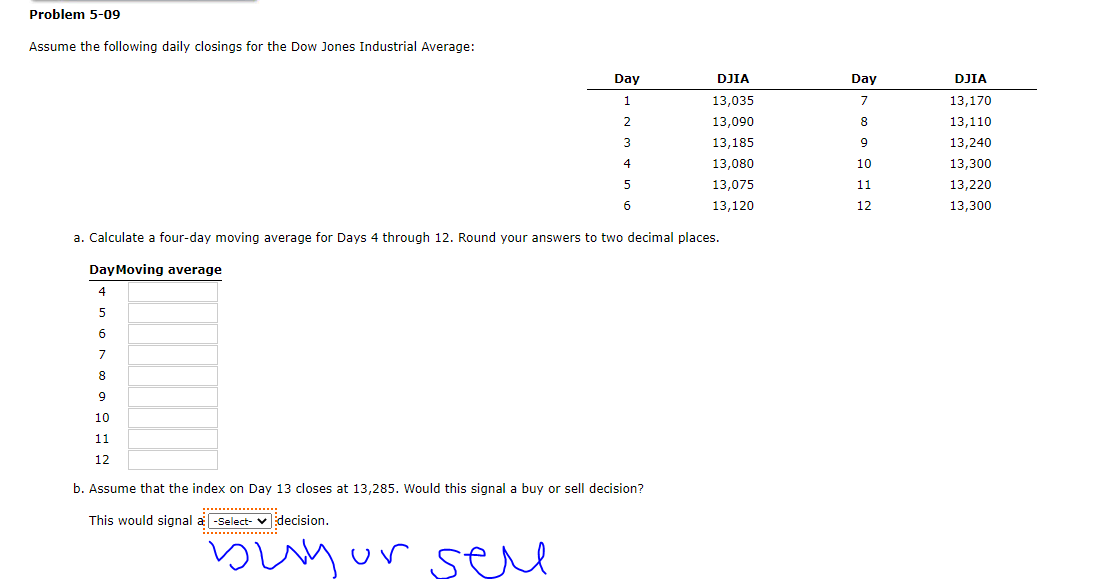

Problem 5-02 Compute the abnormal rates of return for the following stocks assuming the following systematic risk measures (betas): Stock B F Rmt 4.2% 6.8 Rit 12.2% 9.4 15.9 12.9 16.9 Bi 0.80 1.15 1.30 0.70 -0.45 T 5.0 15.9 E 12.9 Rit = return for stock i during period t Rmt = return for the aggregate market during period t B; = beta for stock i Use a minus sign to enter negative values, if any. Round your answers to one decimal place. ARgt % ARFT: % ART: % ARC: % ARE: % Problem 5-09 Assume the following daily closings for the Dow Jones Industrial Average: DJIA Day 1 2 Day 7 8 3 DIA 13,035 13,090 13,185 13,080 13,075 13,120 9 13,170 13,110 13,240 13,300 13,220 13,300 4 10 5 11 6 12 a. Calculate a four-day moving average for Days 4 through 12. Round your answers to two decimal places. Day Moving average 4 5 6 7 8 9 10 11 12 b. Assume that the index on Day 13 closes at 13,285. Would this signal a buy or sell decision? This would signal a -Select- decision. buyur seu

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts