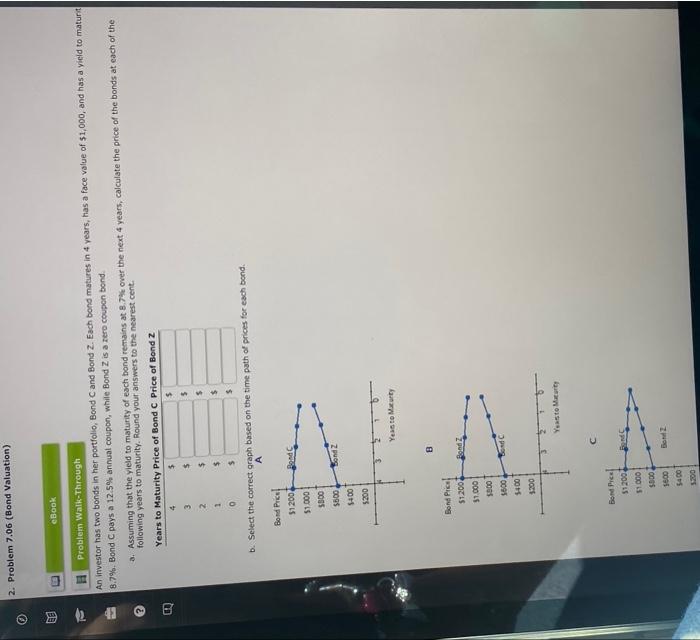

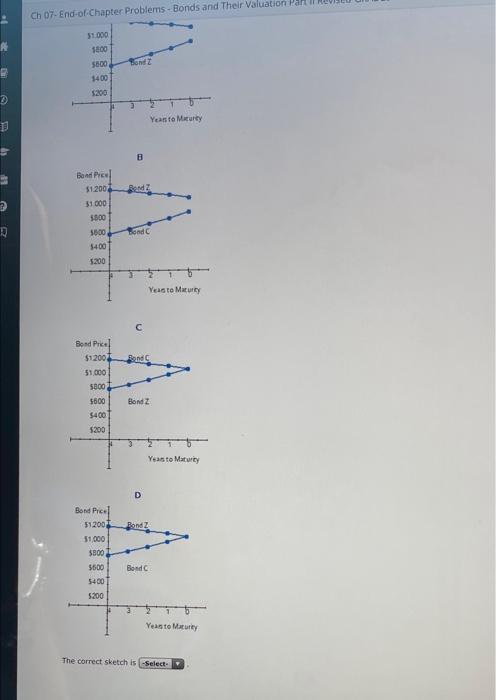

Question: Problem 7.06( Bond Valuation) O 12 2 B 2. Problem 7.06 (Bond Valuation) E eBook H Problem Walk-Through An investor has two bonds in her

O 12 2 B 2. Problem 7.06 (Bond Valuation) E eBook H Problem Walk-Through An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturit 8.7%. Bond C pays a 12.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.7% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Round your answers to the nearest cent. Years to Maturity Price of Bond C Price of Bond Z 4 3 2 1 0 Bond Price $1200 $1.000 $800 $600, $400 $200 Bond Price $1.200 $1.000 1000 $600 $400 $200 $ $ $ $ b. Select the correct graph based on the time path of prices for each bond. A Bond Price $1200 $1.000 $000 1600 $4.00 $300 Bond C Bond Z B Bond Z $ Bond C 5 S $ Year to Maturity Bon $ Yeasto Maturity Ch 07- End-of-Chapter Problems-Bonds and Their Valuation Part II R $1.000 1800 $800 1400 $200 Boad Price $1.200 $1.000 $800 1600 $400 $200 Bond Price $1.200 $1,000 $800 $600 $400 $200 Bond Price $1.200 $1,000 $800 $500 $400 $200 Bond 2 3 B Bend 2 3 Bond C Year to Maturty C Yeas to Maturity Bond C D Bond Z Year to Maturity Bond Z Bond C Year to Maturity The correct sketch is-Select

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts