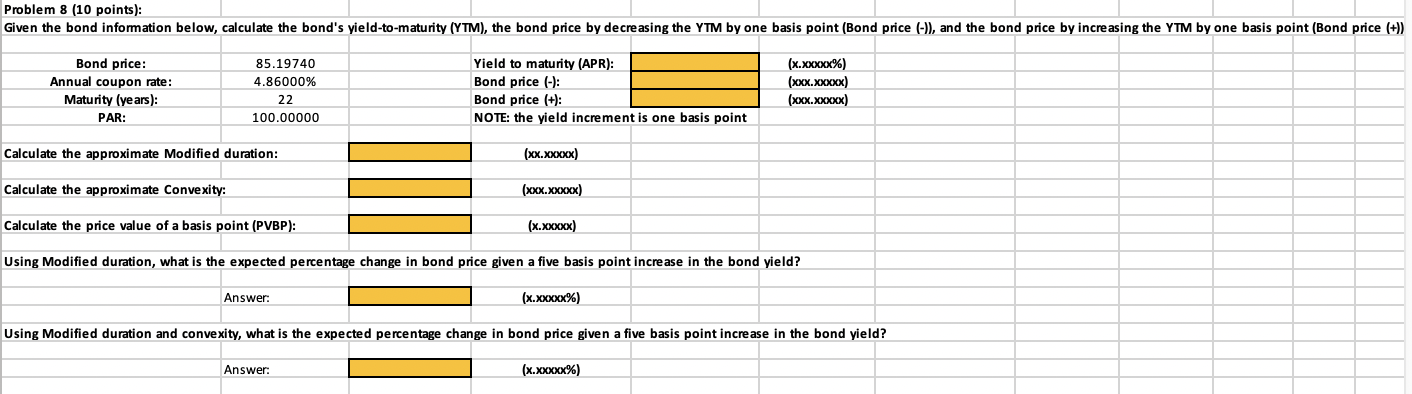

Question: Problem 8 (10 points): Using Modified duration, what is the expected percentage change in bond price given a five basis point increase in the bond

Problem 8 (10 points): Using Modified duration, what is the expected percentage change in bond price given a five basis point increase in the bond yield? \begin{tabular}{l|l|} Answer: & (x.xxxxx\%) \end{tabular} Using Modified duration and convexity, what is the expected percentage change in bond price given a five basis point increase in the bond yield? Answer: (x.xxxxx\%)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock