Question: Process Costing using the FIFO Method A process cost system is used when a company produces a product that is homogeneous-that is, individual units are

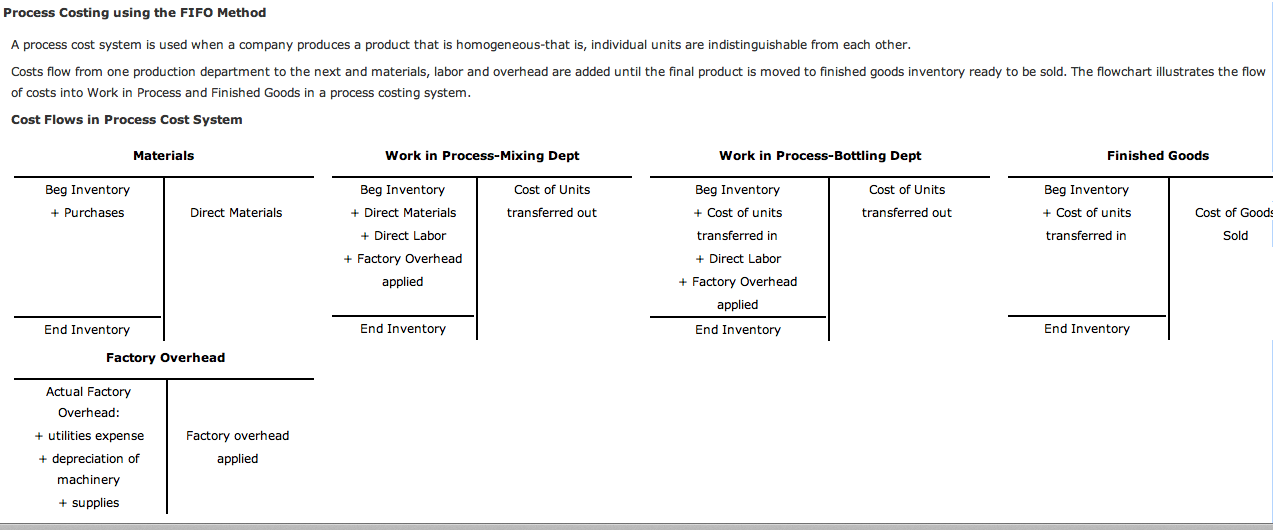

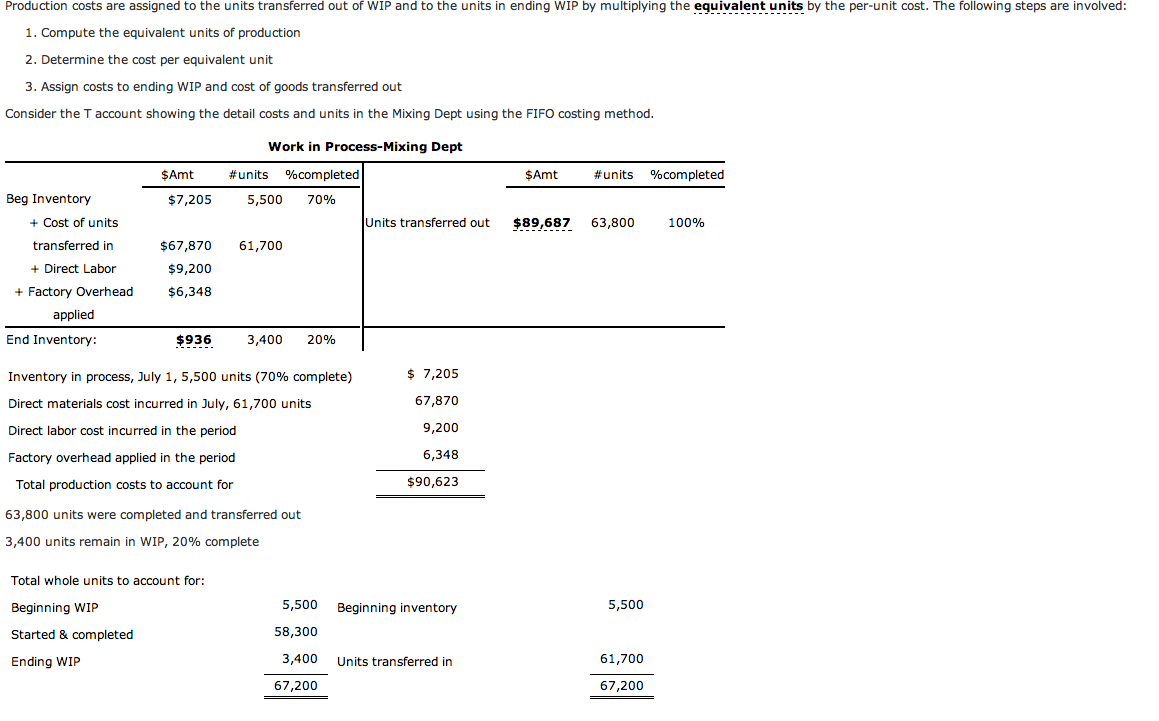

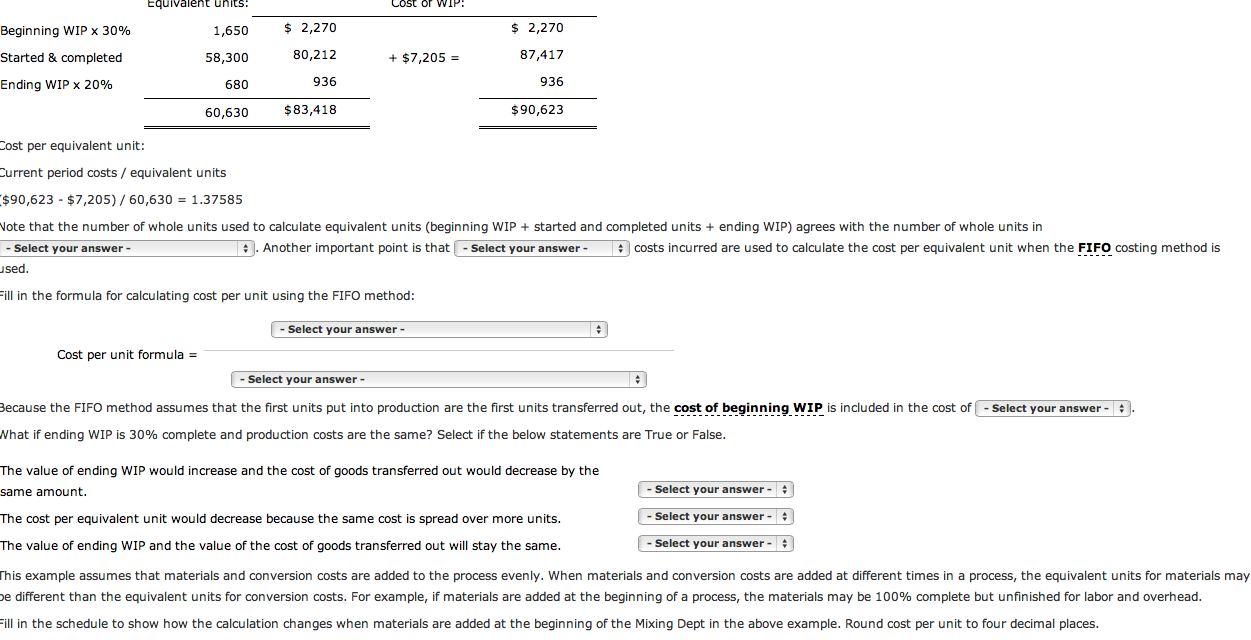

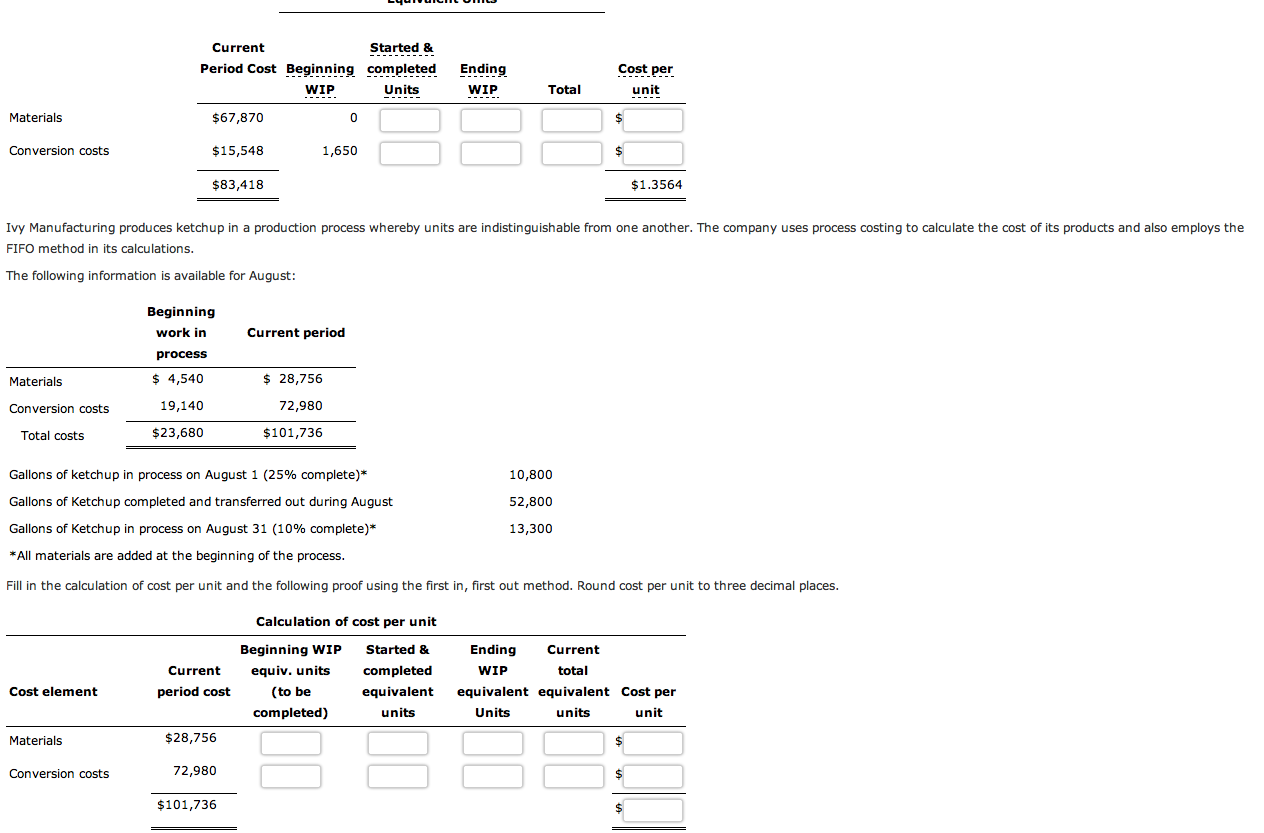

Process Costing using the FIFO Method A process cost system is used when a company produces a product that is homogeneous-that is, individual units are indistinguishable from each other Costs flow from one production department to the next and materials, labor and overhead are added until the final product is moved to finished goods inventory ready to be sold. The flowchart illustrates the flow of costs into Work in Process and Finished Goods in a process costing system Cost Flows in Process Cost System Materials Work in Process-Mixing Dept Work in Process-Bottling Dept Finished Goods Beg Inventory Cost of Units Cost of Units Beg Inventory + Direct Materials + Direct Labor + Factory Overhead applied Beg Inventory + Cost of units transferred in + Direct Labor + Factory Overhead applied End Inventory Beg Inventory + Cost of units transferred in +Purchases Direct Materials transferred out transferred out Cost of Good Sold End Inventory End Inventory End Inventory Factory Overhead Actual Factory Overhead: + utilities expense + depreciation of machinery + supplies Factory overhead applied

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts