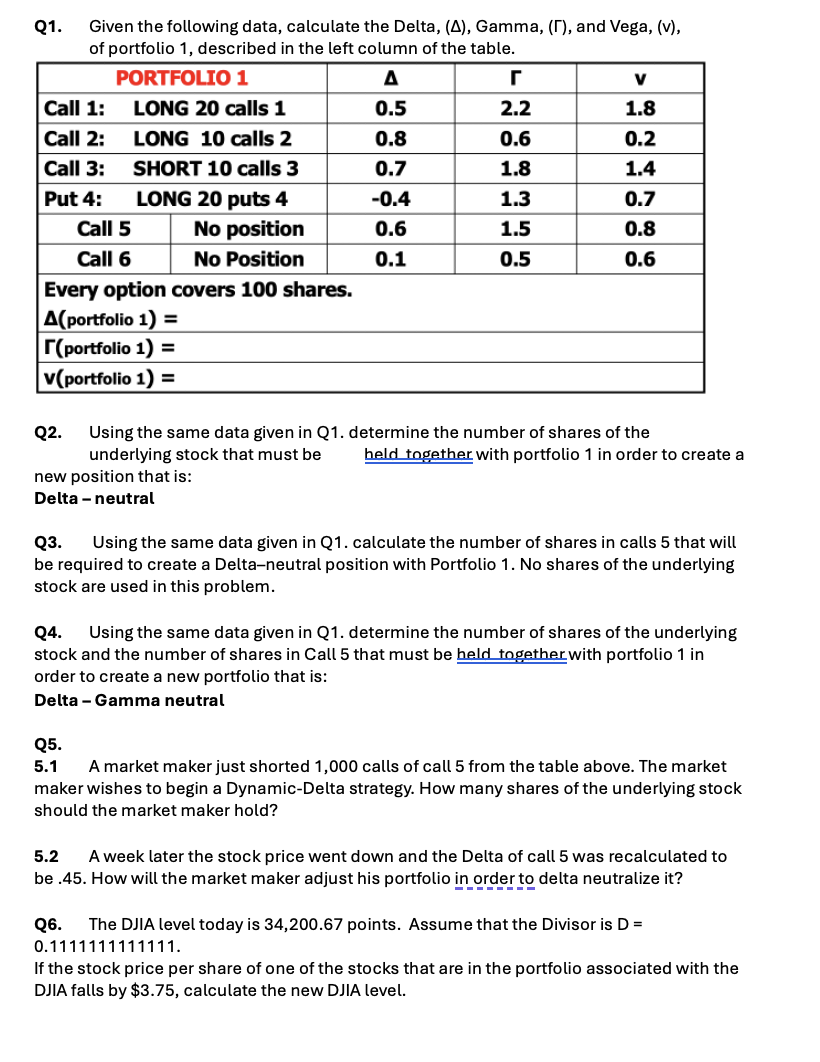

Question: Q 1 . Given the following data, calculate the Delta, ( ) , Gamma, ( , and Vega, ( v ) , of portfolio 1

Q Given the following data, calculate the Delta, Gamma, and Vega, v

of portfolio described in the left column of the table.

Q Using the same data given in Q determine the number of shares of the

underlying stock that must be

held together with portfolio in order to create a

new position that is:

Delta neutral

Q Using the same data given in Q calculate the number of shares in calls that will

be required to create a Deltaneutral position with Portfolio No shares of the underlying

stock are used in this problem.

Q Using the same data given in Q determine the number of shares of the underlying

stock and the number of shares in Call that must be held together with portfolio in

order to create a new portfolio that is:

Delta Gamma neutral

Q

A market maker just shorted calls of call from the table above. The market

maker wishes to begin a DynamicDelta strategy. How many shares of the underlying stock

should the market maker hold?

A week later the stock price went down and the Delta of call was recalculated to

be How will the market maker adjust his portfolio in order to delta neutralize it

Q The DJA level today is points. Assume that the Divisor is

If the stock price per share of one of the stocks that are in the portfolio associated with the

DJIA falls by $ calculate the new DJIA level.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock