Question: Q 6 . You wish to create a Delta - neutral position with two different puts but without any shares of the underlying assets. The

Q You wish to create a Deltaneutral position with two different puts but without any shares of the underlying

assets. The market premiums of these puts are: and

The value of this portfolio is:

Derive the formula for the relationship between the two calls so as to create a Deltaneutral position. Use the

same method that I used on slide but with only the two calls; no stock shares.

Q A financial institution just sold CBOE of the AUG puts. Use the formula you derived in Q to explain

what position will be taken in the OCT put to create a Deltaneutral portfolio, using no shares of the

underlying asset.

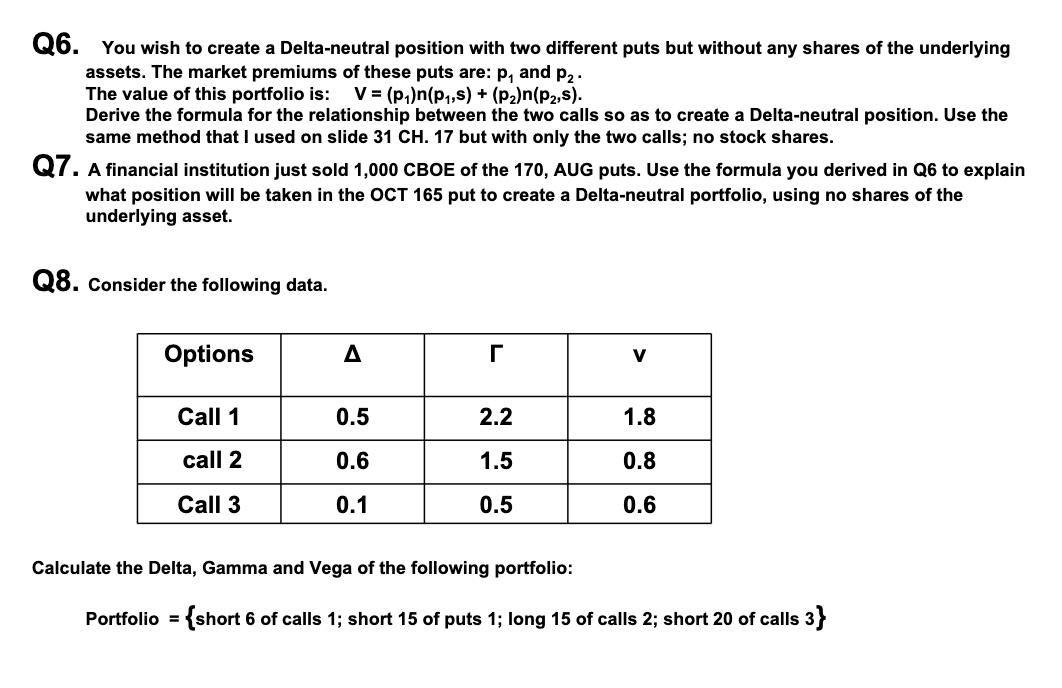

Q Consider the following data.

Calculate the Delta, Gamma and Vega of the following portfolio:

Portfolio short of calls ; short of puts ; long of calls ; short of calls

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock