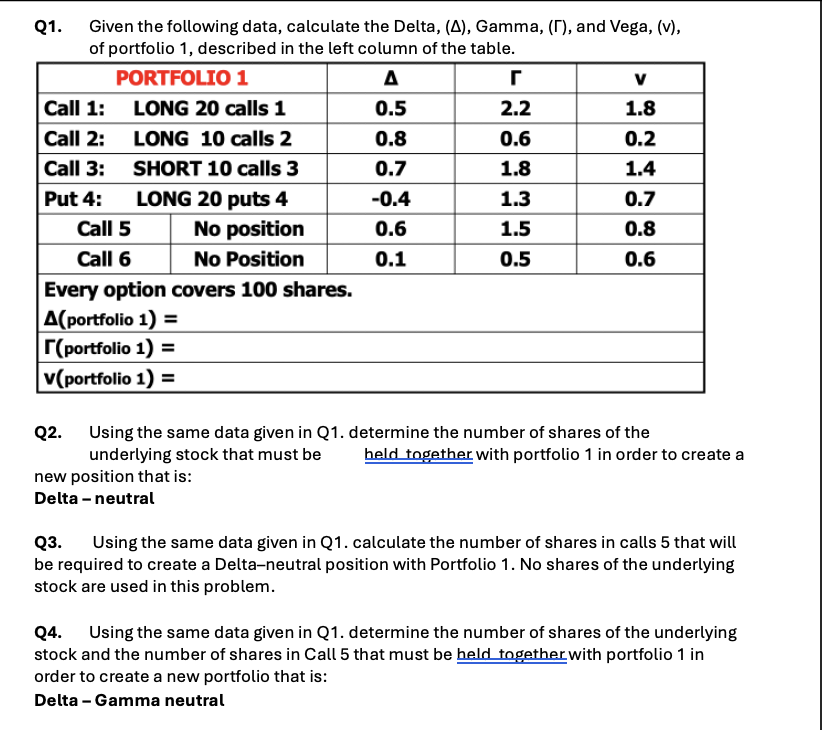

Question: Q 1 . Given the following data, calculate the Delta, ( ) , Gamma, ( ) , and Vega, ( v ) , of portfolio

Q Given the following data, calculate the Delta, Gamma, and Vega, v

of portfolio described in the left column of the table.

Q Using the same data given in Q determine the number of shares of the

underlying stock that must be

held together with portfolio in order to create a

new position that is:

Deltaneutral

Q Using the same data given in Q calculate the number of shares in calls that will

be required to create a Deltaneutral position with Portfolio No shares of the underlying

stock are used in this problem.

Q Using the same data given in Q determine the number of shares of the underlying

stock and the number of shares in Call that must be held together with portfolio in

order to create a new portfolio that is:

DeltaGamma neutral

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock