Question: Q3 part A QUESTION 3 Part A 1. Raw materials inventories are the goods that a manufacturer has completed and are ready to be sold

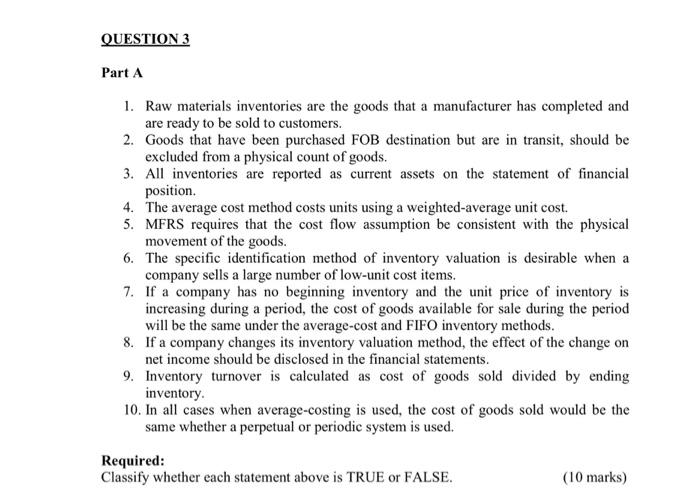

QUESTION 3 Part A 1. Raw materials inventories are the goods that a manufacturer has completed and are ready to be sold to customers. 2. Goods that have been purchased FOB destination but are in transit, should be excluded from a physical count of goods. 3. All inventories are reported as current assets on the statement of financial position. 4. The average cost method costs units using a weighted average unit cost. 5. MERS requires that the cost flow assumption be consistent with the physical movement of the goods. 6. The specific identification method of inventory valuation is desirable when a company sells a large number of low-unit cost items. 7. If a company has no beginning inventory and the unit price of inventory is increasing during a period, the cost of goods available for sale during the period will be the same under the average-cost and FIFO inventory methods. 8. If a company changes its inventory valuation method, the effect of the change on net income should be disclosed in the financial statements. 9. Inventory turnover is calculated as cost of goods sold divided by ending inventory. 10. In all cases when average-costing is used, the cost of goods sold would be the same whether a perpetual or periodic system is used. Required: Classify whether each statement above is TRUE or FALSE. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts