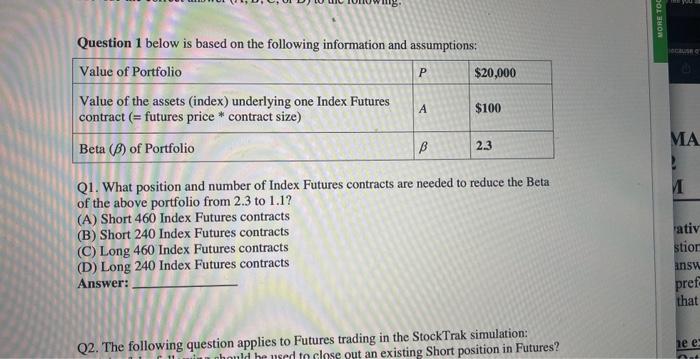

Question: Question 1 below is based on the following information and assumptions: Q1. What position and number of Index Futures contracts are needed to reduce the

Question 1 below is based on the following information and assumptions: Q1. What position and number of Index Futures contracts are needed to reduce the Beta of the above portfolio from 2.3 to 1.1 ? (A) Short 460 Index Futures contracts (B) Short 240 Index Futures contracts (C) Long 460 Index Futures contracts (D) Long 240 Index Futures contracts Answer: Q2. The following question applies to Futures trading in the StockTrak simulation

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock