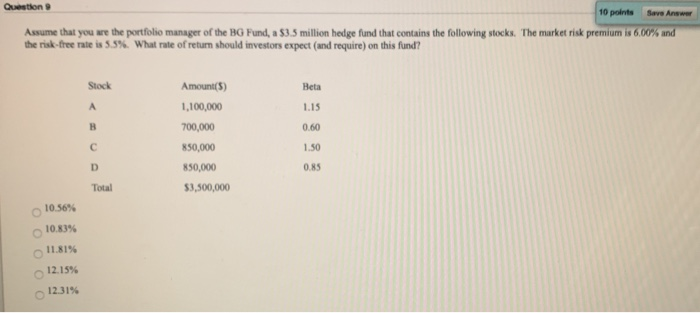

Question: Question 10 points Save Answer Assume that you are the portfolio manager of the BG Fund, a $3.5 million hedge fund that contains the following

Question 10 points Save Answer Assume that you are the portfolio manager of the BG Fund, a $3.5 million hedge fund that contains the following stocks. The market risk premium is 6.00% and the risk-free rate is 5.5%. What rate of return should investors expect and require) on this fund? Stock Beta Amount() 1,100,000 700,000 850,000 850,000 $3,500,000 10.56% 10.83% 11.81% 12.15% 12.31%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock