Question: Question 2 Consider the MSFT option prices below (prices at closing on June 3, 2021). Microsoft current stock price is $247.30 Assume no dividends

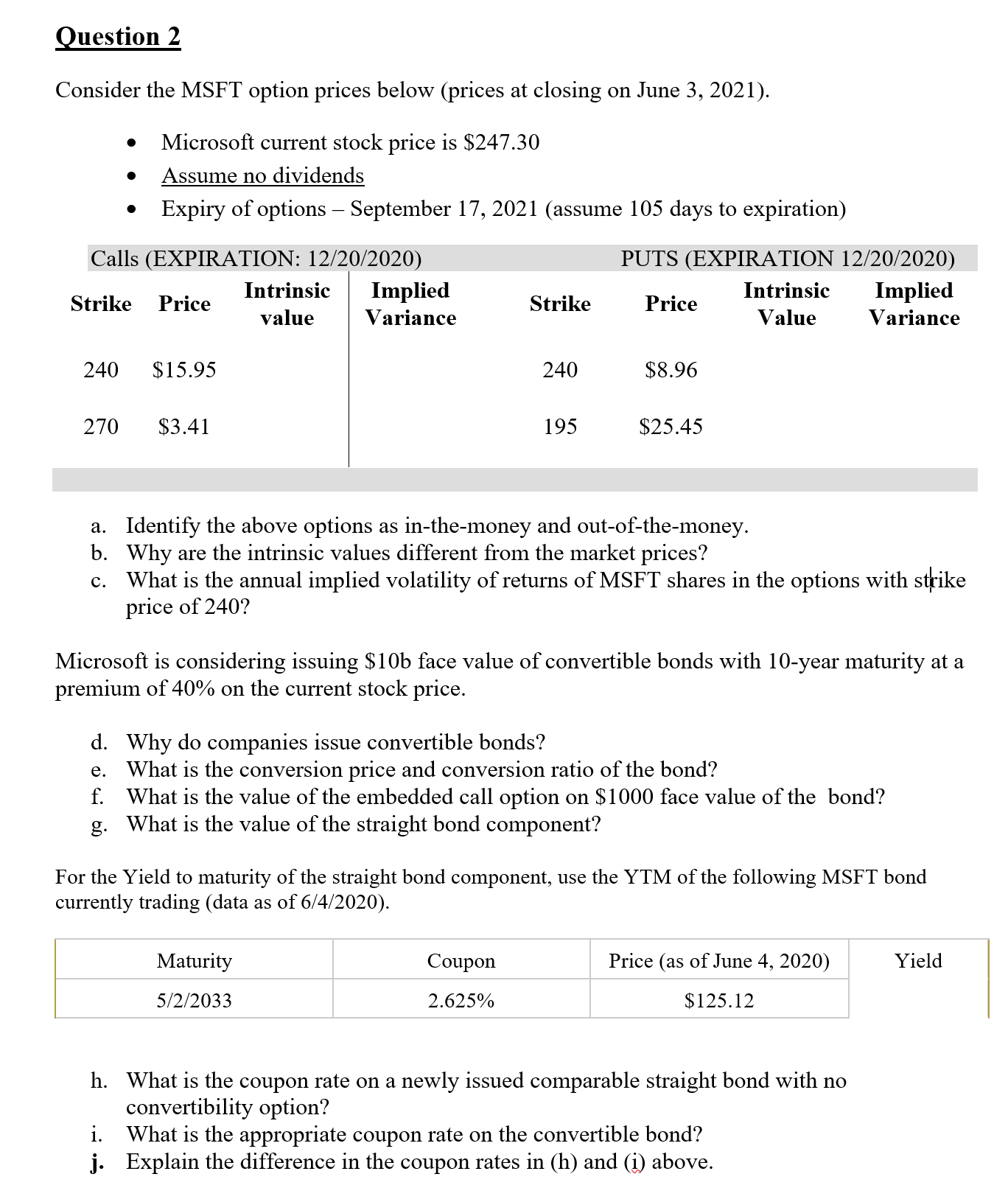

Question 2 Consider the MSFT option prices below (prices at closing on June 3, 2021). Microsoft current stock price is $247.30 Assume no dividends Expiry of options September 17, 2021 (assume 105 days to expiration) - Calls (EXPIRATION: 12/20/2020) Strike Price Intrinsic value 240 $15.95 270 $3.41 PUTS (EXPIRATION 12/20/2020) Implied Variance Strike Price Intrinsic Value Implied Variance 240 $8.96 195 $25.45 a. Identify the above options as in-the-money and out-of-the-money. b. Why are the intrinsic values different from the market prices? c. What is the annual implied volatility of returns of MSFT shares in the options with strike price of 240? Microsoft is considering issuing $10b face value of convertible bonds with 10-year maturity at a premium of 40% on the current stock price. d. Why do companies issue convertible bonds? e. What is the conversion price and conversion ratio of the bond? f. What is the value of the embedded call option on $1000 face value of the bond? g. What is the value of the straight bond component? For the Yield to maturity of the straight bond component, use the YTM of the following MSFT bond currently trading (data as of 6/4/2020). Maturity 5/2/2033 Coupon 2.625% Price (as of June 4, 2020) $125.12 Yield h. What is the coupon rate on a newly issued comparable straight bond with no convertibility option? i. What is the appropriate coupon rate on the convertible bond? j. Explain the difference in the coupon rates in (h) and (i) above.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts