Question: QUESTION 2 The (theta) in the previous question determines the efficient set when it is: a. Minimized b. Constrained cc. Maximized Cd. Not enough information

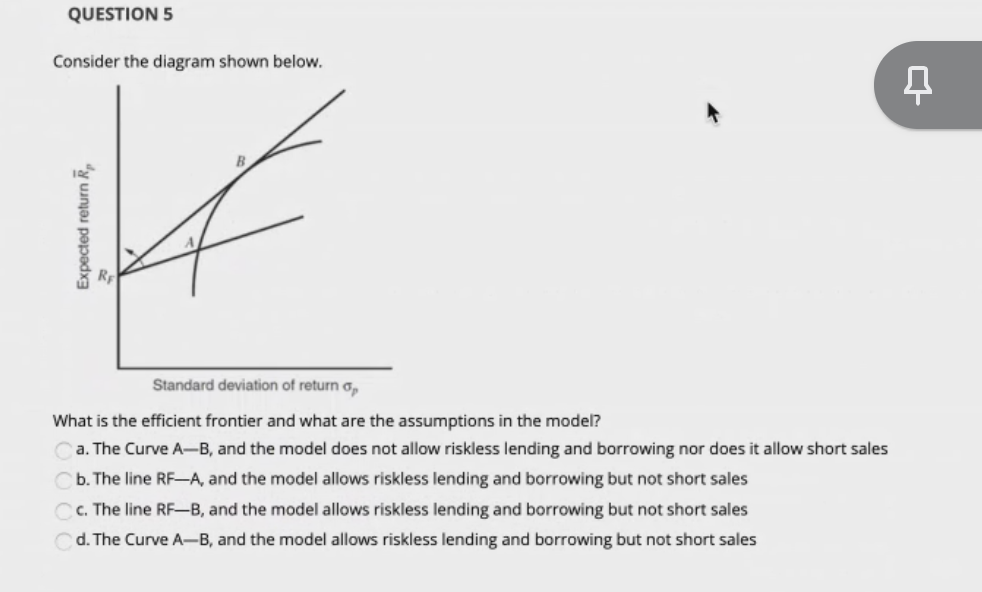

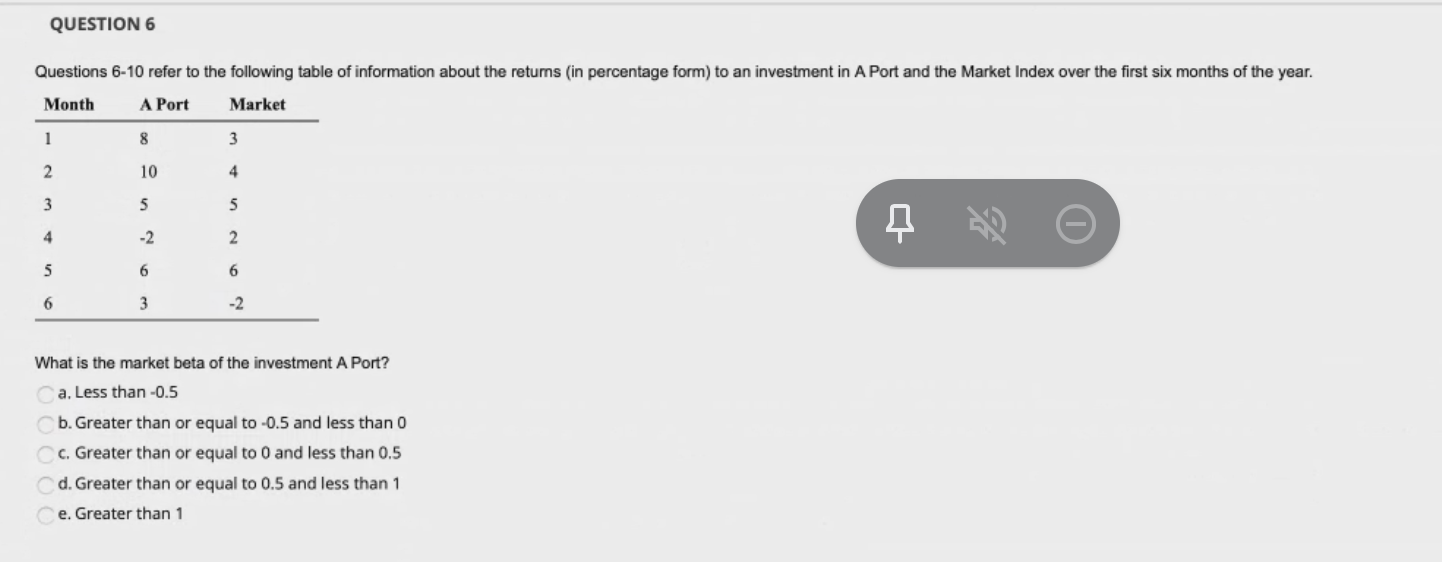

QUESTION 2 The (theta) in the previous question determines the efficient set when it is: a. Minimized b. Constrained cc. Maximized Cd. Not enough information given QUESTION 5 Consider the diagram shown below. it Expected return R Standard deviation of return What is the efficient frontier and what are the assumptions in the model? ca. The Curve A-B, and the model does not allow riskless lending and borrowing nor does it allow short sales b. The line RFA, and the model allows riskless lending and borrowing but not short sales c. The line RF-B, and the model allows riskless lending and borrowing but not short sales d. The Curve A-B, and the model allows riskless lending and borrowing but not short sales QUESTION 6 Questions 6-10 refer to the following table of information about the retums (in percentage form) to an investment in A Port and the Market Index over the first six months of the year. Month A Port Market 1 8 3 2 10 4 3 5 5 0 4 -2 2 5 6 6 6 3 -2 What is the market beta of the investment A Port? a. Less than -0.5 b. Greater than or equal to -0.5 and less than 0 c. Greater than or equal to 0 and less than 0.5 d. Greater than or equal to 0.5 and less than 1 e. Greater than 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts