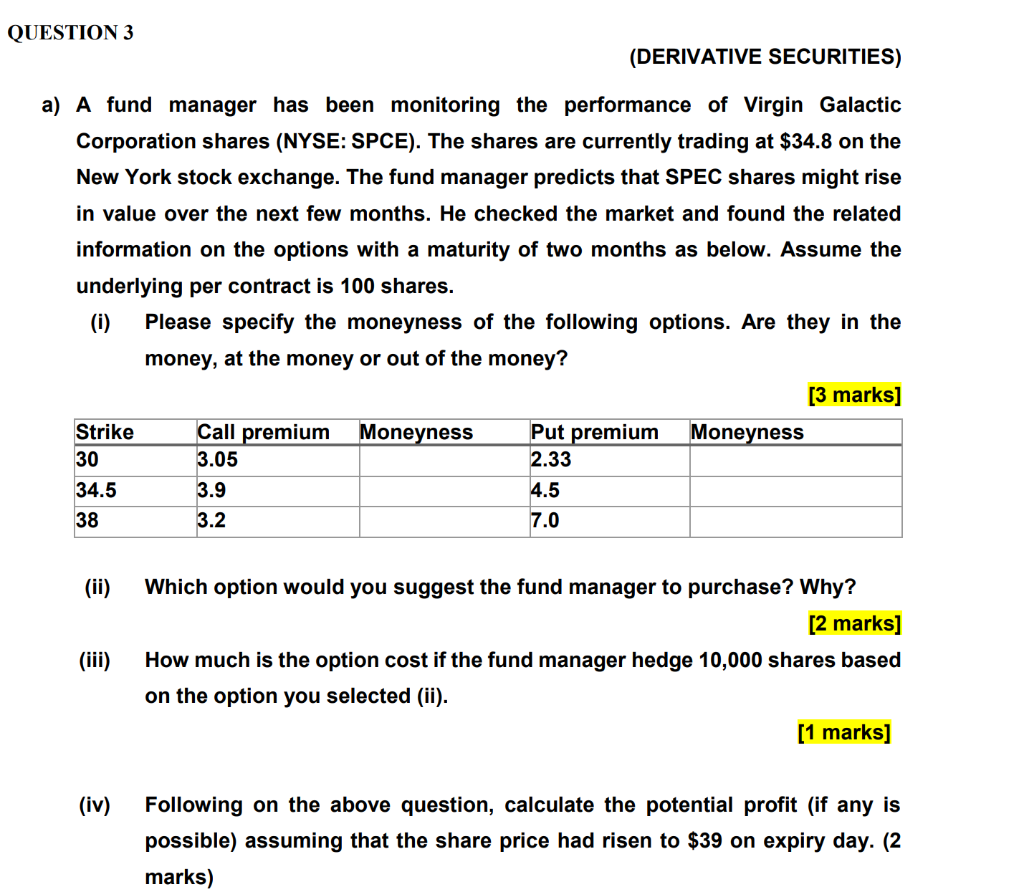

Question: QUESTION 3 (DERIVATIVE SECURITIES) a) A fund manager has been monitoring the performance of Virgin Galactic Corporation shares (NYSE: SPCE). The shares are currently trading

QUESTION 3 (DERIVATIVE SECURITIES) a) A fund manager has been monitoring the performance of Virgin Galactic Corporation shares (NYSE: SPCE). The shares are currently trading at $34.8 on the New York stock exchange. The fund manager predicts that SPEC shares might rise in value over the next few months. He checked the market and found the related information on the options with a maturity of two months as below. Assume the underlying per contract is 100 shares. (0) Please specify the moneyness of the following options. Are they in the money, at the money or out of the money? [3 marks] Strike Call premium Moneyness Put premium Moneyness 30 3.05 2.33 34.5 3.9 4.5 38 3.2 7.0 (iii) Which option would you suggest the fund manager to purchase? Why? [2 marks] How much is the option cost if the fund manager hedge 10,000 shares based on the option you selected (ii). [1 marks] ) (iv) Following on the above question, calculate the potential profit (if any is possible) assuming that the share price had risen to $39 on expiry day. (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts