Question: QUESTION 3 On Jul 1, 2019, P Ltd. acquired a 70% equity stake in S Ltd. for $150,000 and a 30% equity stake in

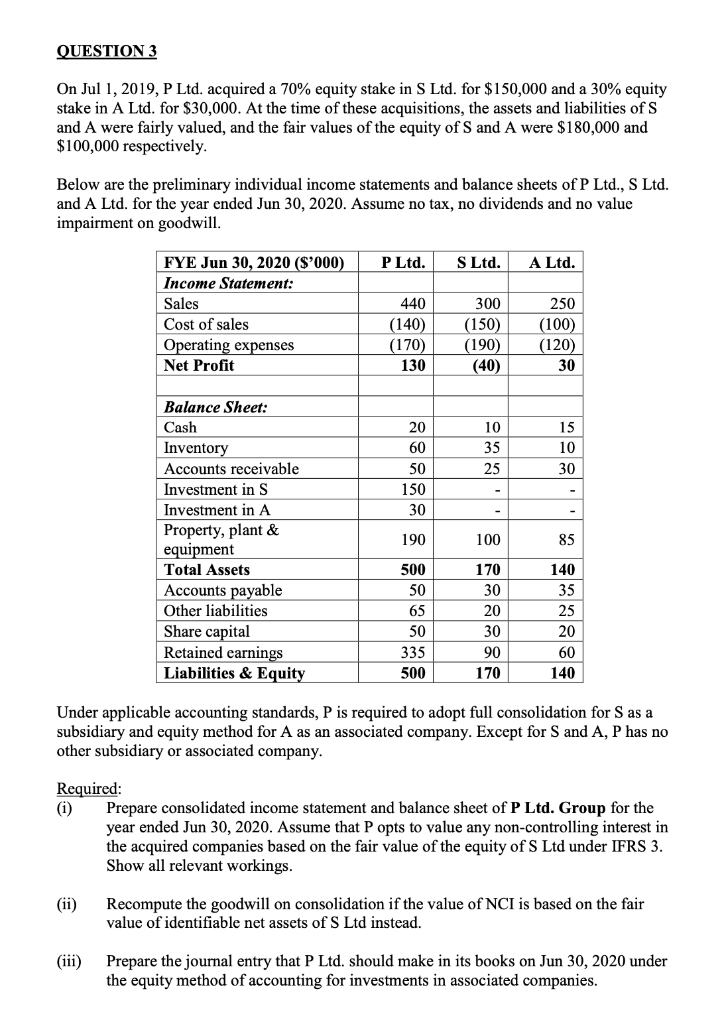

QUESTION 3 On Jul 1, 2019, P Ltd. acquired a 70% equity stake in S Ltd. for $150,000 and a 30% equity stake in A Ltd. for $30,000. At the time of these acquisitions, the assets and liabilities of S and A were fairly valued, and the fair values of the equity of S and A were $180,000 and $100,000 respectively. Below are the preliminary individual income statements and balance sheets of P Ltd., S Ltd. and A Ltd. for the year ended Jun 30, 2020. Assume no tax, no dividends and no value impairment on goodwill. FYE Jun 30, 2020 ($'000) P Ltd. S Ltd. A Ltd. Income Statement: Sales 440 300 250 Cost of sales (140) (150) (100) Operating expenses (170) (190) (120) Net Profit 130 (40) 30 Balance Sheet: Cash 20 10 15 Inventory 60 35 10 Accounts receivable 50 25 30 Investment in S 150 Investment in A 30 - Property, plant & 190 100 equipment Total Assets 500 170 Accounts payable 50 Other liabilities 65 Share capital 50 Retained earnings 335 Liabilities & Equity 500 170 8 232322 30 20 30 90 140 2132284 85 35 25 20 60 Under applicable accounting standards, P is required to adopt full consolidation for S as a subsidiary and equity method for A as an associated company. Except for S and A, P has no other subsidiary or associated company. Required: (i) (ii) Prepare consolidated income statement and balance sheet of P Ltd. Group for the year ended Jun 30, 2020. Assume that P opts to value any non-controlling interest in the acquired companies based on the fair value of the equity of S Ltd under IFRS 3. Show all relevant workings. Recompute the goodwill on consolidation if the value of NCI is based on the fair value of identifiable net assets of S Ltd instead. (iii) Prepare the journal entry that P Ltd. should make in its books on Jun 30, 2020 under the equity method of accounting for investments in associated companies.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts