Question: QUESTION 3 - Risk and Return / Portfolio Theory (30 Marks) The stock market comprises two stocks, A and B, and a risk-free asset. The

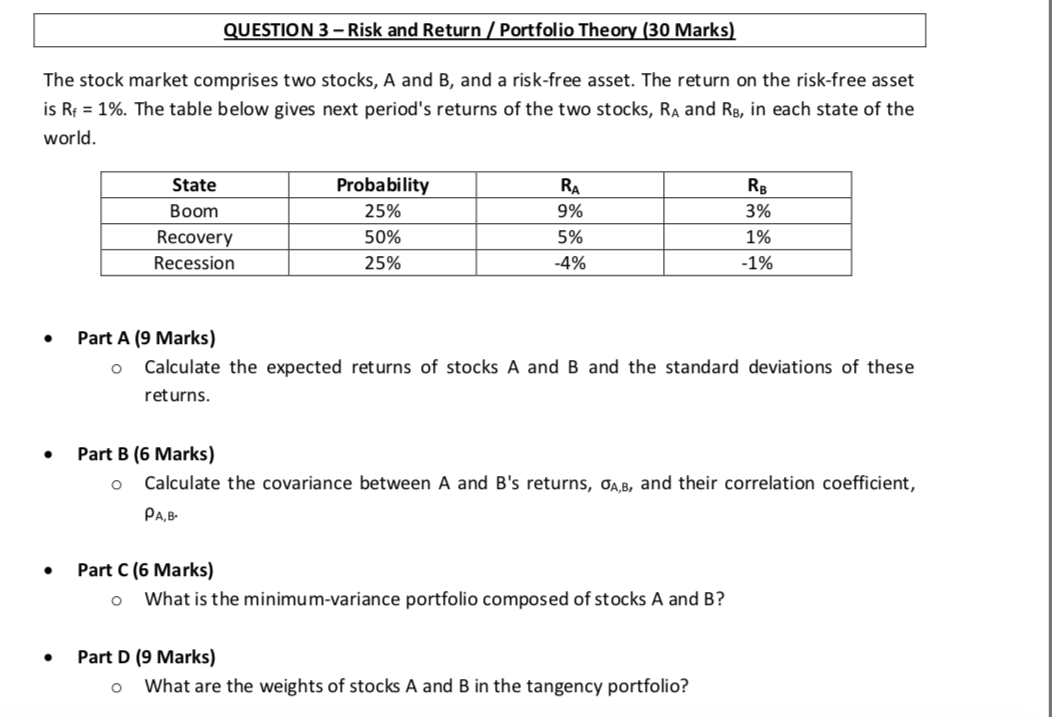

QUESTION 3 - Risk and Return / Portfolio Theory (30 Marks) The stock market comprises two stocks, A and B, and a risk-free asset. The return on the risk-free asset is Rp = 1%. The table below gives next period's returns of the two stocks, RA and RB, in each state of the world. RA RB State Boom Recovery Recession Probability 25% 50% 25% 9% 5% -4% 3% 1% -1% Part A (9 Marks) O Calculate the expected returns of stocks A and B and the standard deviations of these returns. Part B (6 Marks) O Calculate the covariance between A and B's returns, OA,B, and their correlation coefficient, PA,B- Part C (6 Marks) o What is the minimum-variance portfolio composed of stocks A and B? Part D (9 Marks) o What are the weights of stocks A and B in the tangency portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts