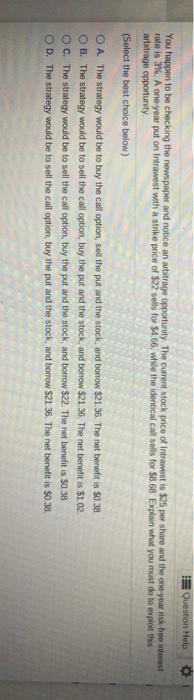

Question: Question Help You happen to be checking the newspaper and notice an arbitrage opportunity. The current stock price of intrawest is $25 por share and

Question Help You happen to be checking the newspaper and notice an arbitrage opportunity. The current stock price of intrawest is $25 por share and the one your risk trointest rate is 3%. A one year put on intrawest with a strike price of $22 sells for $4.66, while the identical cells for $8.68. Explain what you must do to exploit this arbitrage opportunity (Select the best choice below) O A. The strategy would be to buy the call option, sell the put and the stock, and borrow $21.36 The net benefit is $0.3a O B. The strategy would be to sell the call option, buy the put and the stock, and borrow $21.36. The net benefit is $1.02 OC. The strategy would be to sell the call option, buy the put and the stock and borrow $22. The net benefit is $0,38 OD. The strategy would be to sell the call option, buy the put and the stock, and borrow $21.36. The net benatit is $0.38

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts