Question: Questions 1. Duration, Convexity, and Price Approximation (25 points) A specially designed 4-year asset called XYZ generates a series of cash flows as follows (Table

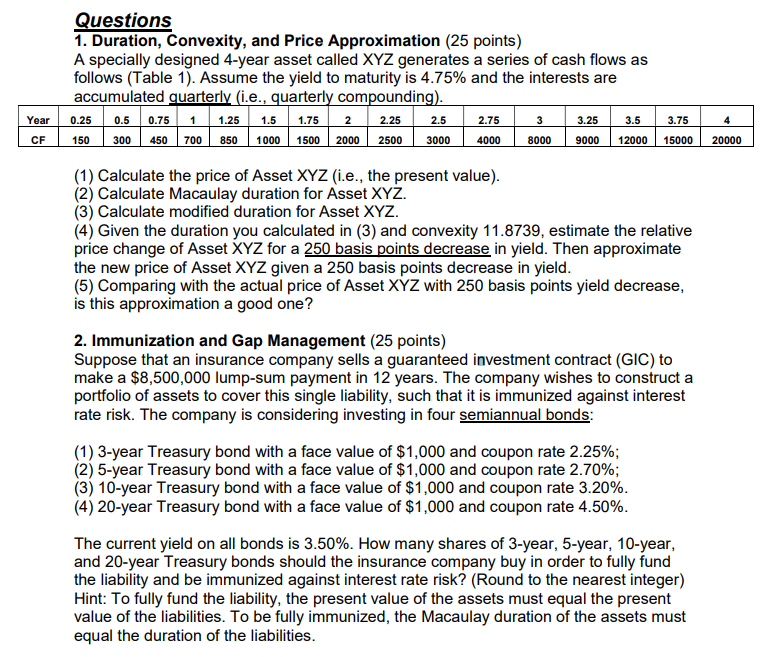

Questions 1. Duration, Convexity, and Price Approximation (25 points) A specially designed 4-year asset called XYZ generates a series of cash flows as follows (Table 1). Assume the yield to maturity is 4.75% and the interests are accumulated quarterly (i.e., quarterly compounding). Year 0.25 0.5 0.75 1 1.25 1.5 1.75 2 2.25 2.5 2.75 3 3.25 3.5 3.75 4 CF 150 300 450 700 850 1000 1500 2000 2500 3000 4000 8000 9000 12000 15000 20000 (1) Calculate the price of Asset XYZ (i.e., the present value). (2) Calculate Macaulay duration for Asset XYZ. (3) Calculate modified duration for Asset XYZ. (4) Given the duration you calculated in (3) and convexity 11.8739, estimate the relative price change of Asset XYZ for a 250 basis points decrease in yield. Then approximate the new price of Asset XYZ given a 250 basis points decrease in yield. (5) Comparing with the actual price of Asset XYZ with 250 basis points yield decrease, is this approximation a good one? 2. Immunization and Gap Management (25 points) Suppose that an insurance company sells a guaranteed investment contract (GIC) to make a $8,500,000 lump-sum payment in 12 years. The company wishes to construct a portfolio of assets to cover this single liability, such that it is immunized against interest rate risk. The company is considering investing in four semiannual bonds: (1) 3-year Treasury bond with a face value of $1,000 and coupon rate 2.25%; (2) 5-year Treasury bond with a face value of $1,000 and coupon rate 2.70%; (3) 10-year Treasury bond with a face value of $1,000 and coupon rate 3.20%. (4) 20-year Treasury bond with a face value of $1,000 and coupon rate 4.50%. The current yield on all bonds is 3.50%. How many shares of 3-year, 5-year, 10-year, and 20-year Treasury bonds should the insurance company buy in order to fully fund the liability and be immunized against interest rate risk? (Round to the nearest integer) Hint: To fully fund the liability, the present value of the assets must equal the present value of the liabilities. To be fully immunized, the Macaulay duration of the assets must equal the duration of the liabilities.

Questions 1. Duration, Convexity, and Price Approximation (25 points) A specially designed 4-year asset called XYZ generates a series of cash flows as follows (Table 1). Assume the yield to maturity is 4.75% and the interests are accumulated quarterly (i.e., quarterly compounding). 0.25 0.5 0.75 1 1.25 1.5 1.75 2 2.25 2.5 2.75 3 3.25 3.5 150 300 450 700 850 1000 1500 2000 2500 3000 4000 8000 9000 12000 Year CF 3.75 15000 4 20000 (1) Calculate the price of Asset XYZ (i.e., the present value). (2) Calculate Macaulay duration for Asset XYZ. (3) Calculate modified duration for Asset XYZ. (4) Given the duration you calculated in (3) and convexity 11.8739, estimate the relative price change of Asset XYZ for a 250 basis points decrease in yield. Then approximate the new price of Asset XYZ given a 250 basis points decrease in yield. (5) Comparing with the actual price of Asset XYZ with 250 basis points yield decrease, is this approximation a good one? 2. Immunization and Gap Management (25 points) Suppose that an insurance company sells a guaranteed investment contract (GIC) to make a $8,500,000 lump-sum payment in 12 years. The company wishes to construct a portfolio of assets to cover this single liability, such that it is immunized against interest rate risk. The company is considering investing in four semiannual bonds: (1) 3-year Treasury bond with a face value of $1,000 and coupon rate 2.25%; (2) 5-year Treasury bond with a face value of $1,000 and coupon rate 2.70%, (3) 10-year Treasury bond with a face value of $1,000 and coupon rate 3.20%. (4) 20-year Treasury bond with a face value of $1,000 and coupon rate 4.50%. The current yield on all bonds is 3.50%. How many shares of 3-year, 5-year, 10-year, and 20-year Treasury bonds should the insurance company buy in order to fully fund the liability and be immunized against interest rate risk? (Round to the nearest integer) Hint: To fully fund the liability, the present value of the assets must equal the present value of the liabilities. To be fully immunized, the Macaulay duration of the assets must equal the duration of the liabilities. Questions 1. Duration, Convexity, and Price Approximation (25 points) A specially designed 4-year asset called XYZ generates a series of cash flows as follows (Table 1). Assume the yield to maturity is 4.75% and the interests are accumulated quarterly (i.e., quarterly compounding). 0.25 0.5 0.75 1 1.25 1.5 1.75 2 2.25 2.5 2.75 3 3.25 3.5 150 300 450 700 850 1000 1500 2000 2500 3000 4000 8000 9000 12000 Year CF 3.75 15000 4 20000 (1) Calculate the price of Asset XYZ (i.e., the present value). (2) Calculate Macaulay duration for Asset XYZ. (3) Calculate modified duration for Asset XYZ. (4) Given the duration you calculated in (3) and convexity 11.8739, estimate the relative price change of Asset XYZ for a 250 basis points decrease in yield. Then approximate the new price of Asset XYZ given a 250 basis points decrease in yield. (5) Comparing with the actual price of Asset XYZ with 250 basis points yield decrease, is this approximation a good one? 2. Immunization and Gap Management (25 points) Suppose that an insurance company sells a guaranteed investment contract (GIC) to make a $8,500,000 lump-sum payment in 12 years. The company wishes to construct a portfolio of assets to cover this single liability, such that it is immunized against interest rate risk. The company is considering investing in four semiannual bonds: (1) 3-year Treasury bond with a face value of $1,000 and coupon rate 2.25%; (2) 5-year Treasury bond with a face value of $1,000 and coupon rate 2.70%, (3) 10-year Treasury bond with a face value of $1,000 and coupon rate 3.20%. (4) 20-year Treasury bond with a face value of $1,000 and coupon rate 4.50%. The current yield on all bonds is 3.50%. How many shares of 3-year, 5-year, 10-year, and 20-year Treasury bonds should the insurance company buy in order to fully fund the liability and be immunized against interest rate risk? (Round to the nearest integer) Hint: To fully fund the liability, the present value of the assets must equal the present value of the liabilities. To be fully immunized, the Macaulay duration of the assets must equal the duration of the liabilities

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts