Read the Case Study: Nortel Networks Corporation: Ethical missteps. After reading the case study, describe the ethical

Fantastic news! We've Found the answer you've been seeking!

Question:

Read the Case Study: Nortel Networks Corporation: Ethical missteps.

- After reading the case study, describe the ethical breach that was entered into by leadership at Nortel.

- Use the three components of the Fraud Triangle to evaluate the actions of the leadership.

- Describe how the tone at the top contributed to this fraudulent activity.

- How did the Audit Committee and Board fail in their responsibilities?

- Describe how various stakeholders (employees, stockholders, and the community) would have been affected by the actions of those in leadership.

Transcribed Image Text:

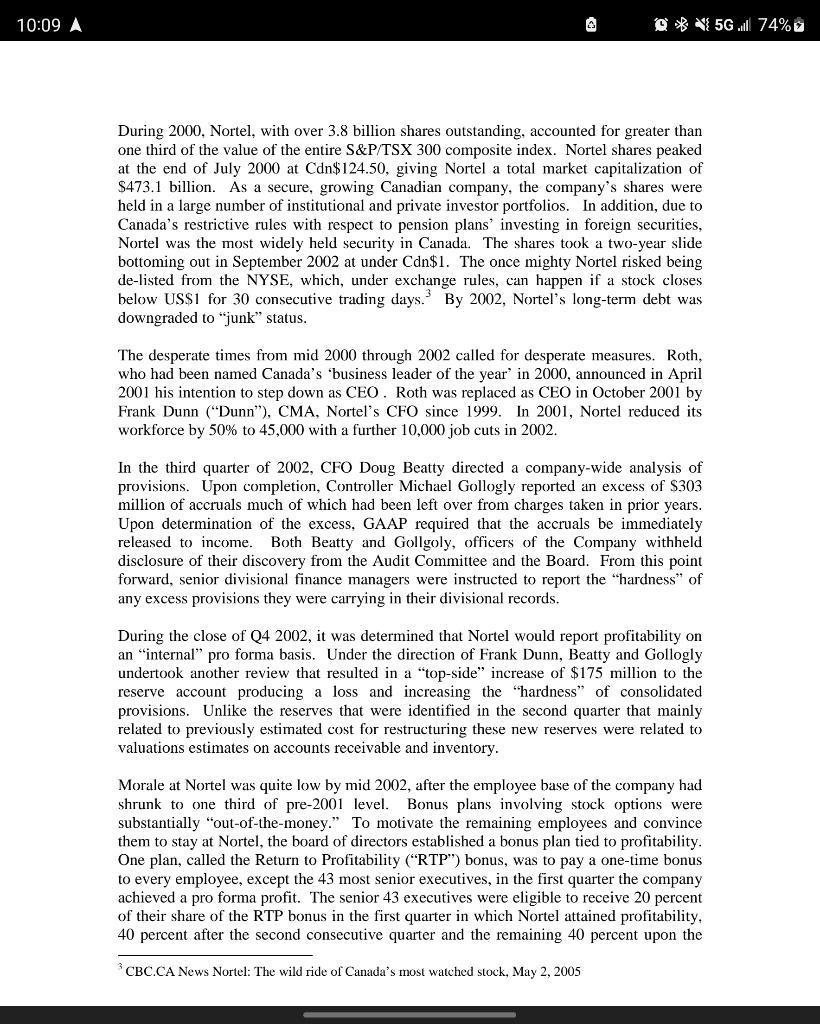

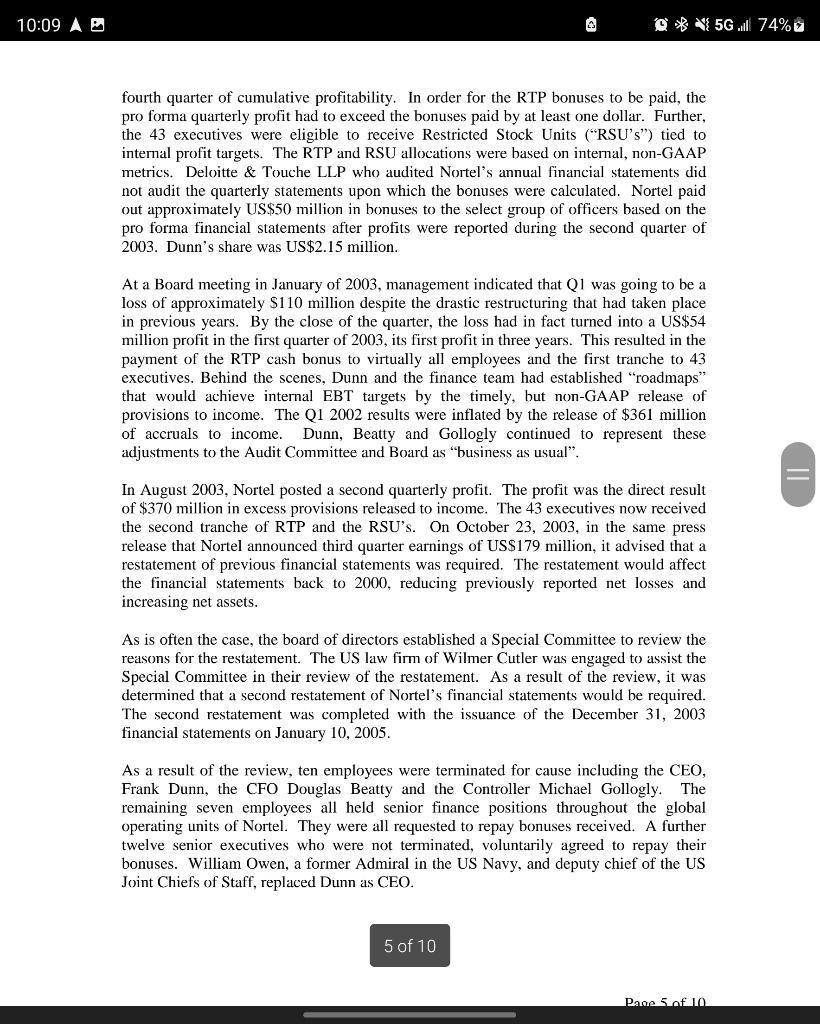

10:09 A O * N 5G ill 74% During 2000, Nortel, with over 3.8 billion shares outstanding, accounted for greater than one third of the value of the entire S&P/TSX 300 composite index. Nortel shares peaked at the end of July 2000 at Cdn$124.50, giving Nortel a total market capitalization of $473.1 billion. As a secure, growing Canadian company, the company's shares were held in a large number of institutional and private investor portfolios. In addition, due to Canada's restrictive rules with respect to pension plans' investing in foreign securities, Nortel was the most widely held security in Canada. The shares took a two-year slide bottoming out in September 2002 at under Cdn$1. The once mighty Nortel risked being de-listed from the NYSE, which, under exchange rules, can happen if a stock closes below US$1 for 30 consecutive trading days. By 2002, Nortel's long-term debt was downgraded to "junk" status. The desperate times from mid 2000 through 2002 called for desperate measures. Roth, who had been named Canada's 'business leader of the year' in 2000, announced in April 2001 his intention to step down as CEO. Roth was replaced as CEO in October 2001 by Frank Dunn ("Dunn"), CMA, Nortel's CFO since 1999. In 2001, Nortel reduced its workforce by 50% to 45,000 with a further 10,000 job cuts in 2002. In the third quarter of 2002, CFO Doug Beatty directed a company-wide analysis of provisions. Upon completion, Controller Michael Gollogly reported an excess of $303 million of accruals much of which had been left over from charges taken in prior years. Upon determination of the excess, GAAP required that the accruals be immediately released to income. Both Beatty and Gollgoly, officers of the Company withheld disclosure of their discovery from the Audit Committee and the Board. From this point forward, senior divisional finance managers were instructed to report the "hardness" of any excess provisions they were carrying in their divisional records. During the close of Q4 2002, it was determined that Nortel would report profitability on an "internal" pro forma basis. Under the direction of Frank Dunn, Beatty and Gollogly undertook another review that resulted in a "top-side" increase of $175 million to the reserve account producing a loss and increasing the "hardness" of consolidated provisions. Unlike the reserves that were identified in the second quarter that mainly related to previously estimated cost for restructuring these new reserves were related to valuations estimates on accounts receivable and inventory. Morale at Nortel was quite low by mid 2002, after the employee base of the company had shrunk to one third of pre-2001 level. Bonus plans involving stock options were substantially "out-of-the-money." To motivate the remaining employees and convince them to stay at Nortel, the board of directors established a bonus plan tied to profitability. One plan, called the Return to Profitability ("RTP") bonus, was to pay a one-time bonus to every employee, except the 43 most senior executives, in the first quarter the company achieved a pro forma profit. The senior 43 executives were eligible to receive 20 percent of their share of the RTP bonus in the first quarter 40 percent after the second consecutive quarter and the remaining 40 percent upon the which Nortel attained profitability, CBC.CA News Nortel: The wild ride of Canada's most watched stock, May 2, 2005 10:09 A O * N 5G ill 74% During 2000, Nortel, with over 3.8 billion shares outstanding, accounted for greater than one third of the value of the entire S&P/TSX 300 composite index. Nortel shares peaked at the end of July 2000 at Cdn$124.50, giving Nortel a total market capitalization of $473.1 billion. As a secure, growing Canadian company, the company's shares were held in a large number of institutional and private investor portfolios. In addition, due to Canada's restrictive rules with respect to pension plans' investing in foreign securities, Nortel was the most widely held security in Canada. The shares took a two-year slide bottoming out in September 2002 at under Cdn$1. The once mighty Nortel risked being de-listed from the NYSE, which, under exchange rules, can happen if a stock closes below US$1 for 30 consecutive trading days. By 2002, Nortel's long-term debt was downgraded to "junk" status. The desperate times from mid 2000 through 2002 called for desperate measures. Roth, who had been named Canada's 'business leader of the year' in 2000, announced in April 2001 his intention to step down as CEO. Roth was replaced as CEO in October 2001 by Frank Dunn ("Dunn"), CMA, Nortel's CFO since 1999. In 2001, Nortel reduced its workforce by 50% to 45,000 with a further 10,000 job cuts in 2002. In the third quarter of 2002, CFO Doug Beatty directed a company-wide analysis of provisions. Upon completion, Controller Michael Gollogly reported an excess of $303 million of accruals much of which had been left over from charges taken in prior years. Upon determination of the excess, GAAP required that the accruals be immediately released to income. Both Beatty and Gollgoly, officers of the Company withheld disclosure of their discovery from the Audit Committee and the Board. From this point forward, senior divisional finance managers were instructed to report the "hardness" of any excess provisions they were carrying in their divisional records. During the close of Q4 2002, it was determined that Nortel would report profitability on an "internal" pro forma basis. Under the direction of Frank Dunn, Beatty and Gollogly undertook another review that resulted in a "top-side" increase of $175 million to the reserve account producing a loss and increasing the "hardness" of consolidated provisions. Unlike the reserves that were identified in the second quarter that mainly related to previously estimated cost for restructuring these new reserves were related to valuations estimates on accounts receivable and inventory. Morale at Nortel was quite low by mid 2002, after the employee base of the company had shrunk to one third of pre-2001 level. Bonus plans involving stock options were substantially "out-of-the-money." To motivate the remaining employees and convince them to stay at Nortel, the board of directors established a bonus plan tied to profitability. One plan, called the Return to Profitability ("RTP") bonus, was to pay a one-time bonus to every employee, except the 43 most senior executives, in the first quarter the company achieved a pro forma profit. The senior 43 executives were eligible to receive 20 percent of their share of the RTP bonus in the first quarter 40 percent after the second consecutive quarter and the remaining 40 percent upon the which Nortel attained profitability, CBC.CA News Nortel: The wild ride of Canada's most watched stock, May 2, 2005

Expert Answer:

Answer rating: 100% (QA)

1 After reading the case study describe the ethical breac... View the full answer

Posted Date:

Students also viewed these accounting questions

-

Read the case study "Business Plan for Room for Desert Adding Unique Ingredients to Life Balancing" and address the following: a) After evaluating the business plan for Room for dessert. What are...

-

Read the Case Study "Improving a commercial bank's operation performance through statistical process control" and respond to threaten discussion 1. The paper states that after elimination of special...

-

Read the case study titled "Pre-Launch decisions which influence innovation success". Write a paper in which the following items are addressed. Discuss the necessity of short-term and long-term...

-

Given, R = 192 R = 22 C=2F C=4F (1) V www R www R R R C The time constants (in S) for the circuits I, II, III are respectively (A) 18, 8/9, 4 (C) 4, 8/9, 18 (II) (B) 18, 4, 8/9 (D) 8/9, 18, 4 R3 (III)

-

According to the Bureau of Labor Statistics, the average hourly wage in the United States was $ 22.57 in May 2010. To confirm this wage, a random sample of 36 hourly workers was selected during the...

-

Sharon transfers to Russ a life insurance policy with cash surrender value of $30,000 and a face value of $100,000 in exchange for real estate. Russ continues to pay the premiums on the policy until...

-

Show that \[S S_{T}=S S_{\text {Treat }}+S S_{E},\] where $S S_{T}=\sum_{i=1}^{k} \sum_{j=1}^{n_{i}}\left(y_{i j}-\bar{y} . ight)^{2}, S S_{\text {Treat }}=\sum_{i=1}^{k}...

-

VSOP, Inc., has a number of divisions that produce liquors, malt beverages, and glassware. The Glassware Division manufactures a variety of bottles that can be sold externally (to soft-drink and...

-

On January 1, 2021, Entity A Company acquired all the assets and assumed all the liabilities of Entity B Company and merged Entity B into Entity A. In exchange for the net assets of Entity B, Entity...

-

Jack Tasker opened his Auto Repair Shop in November 2023. The balance sheet at November 30, 2023, prepared by an inexperienced part-time bookkeeper, is shown below. Required Prepare a correct balance...

-

To calculate effective gross income in the presence of miscellaneous income, vacancy and collection losses are. subtracted from potential gross income added to potential gross income ignored in the...

-

Using the Shewhart charting methods described in Figure 2.4 in Chapter 2, analyze the performance of the following invoice processing activity. The standard time to validate an invoice for payment is...

-

Use the graph of the rational function in the figure shown to complete each statement in Exercises 914. Vortical asymptoto: x = -3 Horizontal asymptoto: y = 0 -3 -2 -1 y 3+ 2+ -2- -3- 2 3 X Vertical...

-

Use the graph of the rational function in the figure shown to complete each statement in Exercises 914. Vortical asymptoto: x = -3 Horizontal asymptoto: y = 0 -3 -2 -1 y 3+ 2+ -2- -3- 2 3 X Vertical...

-

The stacked plot in Figure 3.20 shows the numbers of higher education students enrolled in public and private colleges. The last few bars are projections from the U.S. National Center for Education...

-

The accompanying graph indicates the amount of time (latency) that female subjects were willing to leave their hand in icy water while they were swearing (words you might use after hitting yourself...

-

Frank supervises numerous employees, including Irene. On one project during the year, Irene made a small mistake that cost the company money. Six months later, and shortly before completing Irene's...

-

Solve each equation. x 3 - 6x 2 = -8x

-

In this chapter, we had only expressed eigenstates of the harmonic oscillator Hamiltonian through repeated action of the raising operator, \(\hat{a}^{\dagger}\). This gives us a concrete algorithm...

-

In this chapter, we noted that the Hilbert space of the harmonic oscillator corresponds to all those states that can be accessed from the ground state through action by an anatic function of...

-

Supersymmetry is a proposed extension of the symmetries of space-time beyond that of just familiar Lorentz transformations and translations. A supersymmetry transformation interchanges fermions and...

Wild Chimpanzees Social Behavior Of An Endangered Species 1st Edition - ISBN: 1316647560 - Free Book

Study smarter with the SolutionInn App