Question: Replicate in a working spreadsheet the Exhibit below and provide the price of the bond based on the cashflows. Exhibit 4.5 Calculation of Macaulay Duration

Replicate in a working spreadsheet the Exhibit below and provide the price of the bond based on the cashflows.

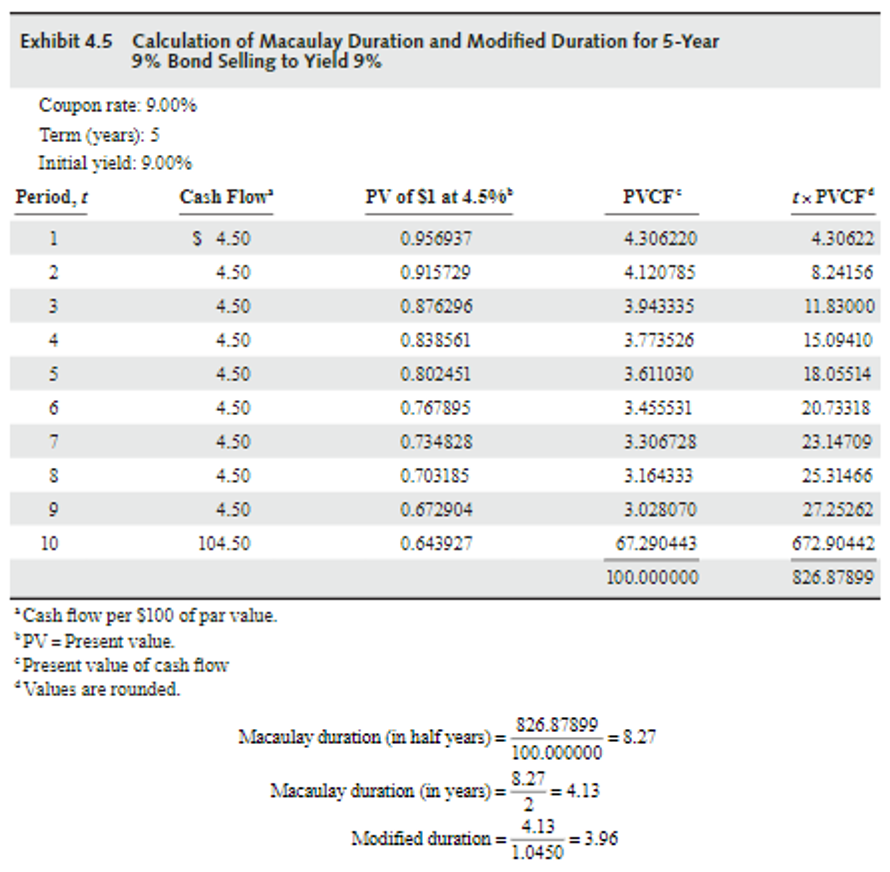

Exhibit 4.5 Calculation of Macaulay Duration and Modified Duration for 5-Year 9% Bond Selling to Yield 9% Coupon rate: 0.00% Term (years): 5 Initial yield: 9.00% Period, Cash Flow PV of S1 at 4.596 PVCF Ex PVCF- 1 $ 4.50 4.30622 2 3 0.956937 0.915729 0.876296 4.50 4.50 4.50 8.24156 4.306220 4.120785 3.943335 11.83000 0.838561 3.773526 15.09410 5 4.50 3.611030 18.05514 0.802451 0.767895 6 20.73318 4.50 4.50 3.455531 3.306728 7 23.14709 0.734828 0.703185 8 4.50 3.164333 25.31466 9 0.672904 3.028070 27.25262 4.50 104.50 10 0.643927 67.290443 672.90442 100.000000 826.87899 Cash flow per $100 of par value. PV = Present value. Present value of cash flow Values are rounded. 826.87899 Macaulay churation (in half years) = = 3.27 100.000000 8.27 Macaulay duration in years) = = 4.13 2 4.13 Modified duration= = 3.96 1.0450

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts