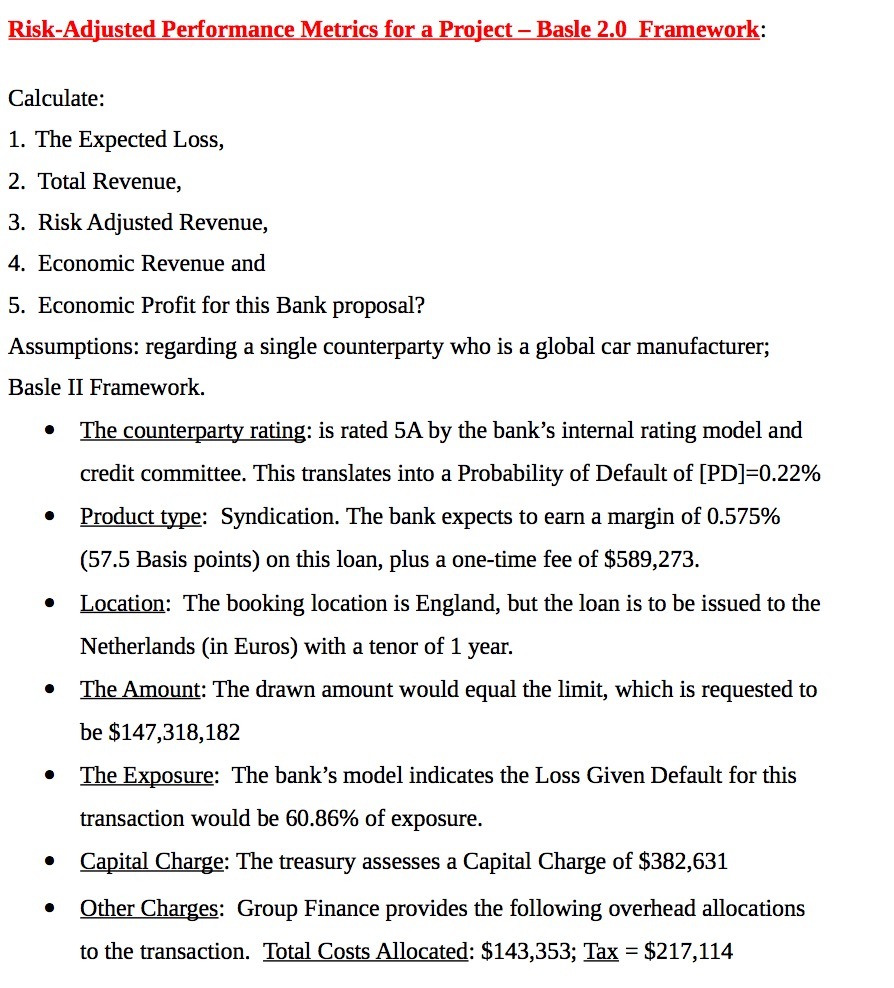

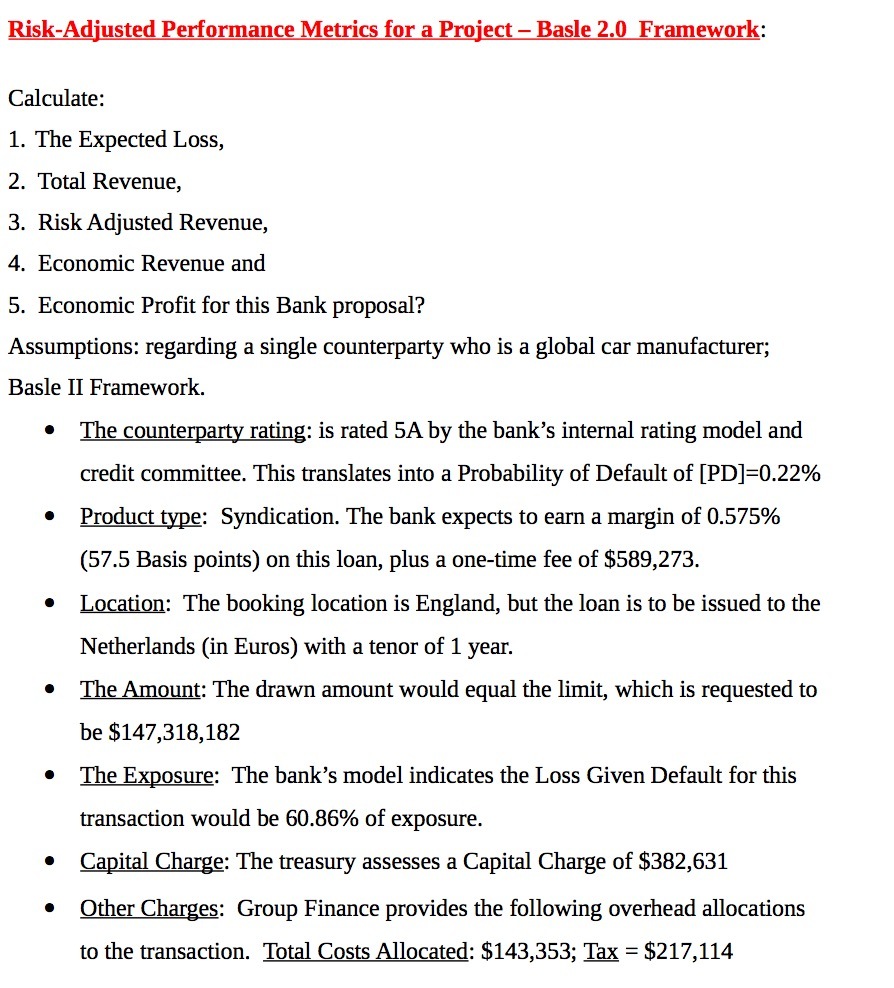

Question: Risk-Adjusted Performance Metrig for a Project Basle 2.0 Framework: Calculate: . The Expected Loss, . Total Revenue, . Economic Revenue and 1 2 3. Risk

Risk-Adjusted Performance Metrig for a Project Basle 2.0 Framework: Calculate: . The Expected Loss, . Total Revenue, . Economic Revenue and 1 2 3. Risk Adjusted Revenue, 4 5 . Economic Prot for this Bank proposal? Assumptions: regarding a single counterparty who is a global car manufacturer; Basle II Framework. The countermrjy rating: is rated 5A by the bank's internal rating model and credit committee. This 1Ianslates into a Probability of Default of [PD]=0.22% Product gape: Syndication. The bank expects to earn a margin of 0.575% (57.5 Basis points) on this loan, plus a one-time fee of $539,273. Location: The booking location is England, but the loan is to be issued to the Netherlands (in Euros) with a tenor of 1 year. The Amount: The drawn amount would equal the limit, which is requested to be $147,318,182 The Exposure: The bank's model indicates the Loss Given Default for this transaction would be 60.36% of exposure. Capital Charge: The treasury assesses a Capital Charge of $382,631 Other Charges: Group Finance provides the following overhead allocations to the transaction. Total Costs Allocated: $143,353; m = $217,114

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts