Question: SINGLE INDEXMODEL The standard form of portfolio solution involves exiensive data needs, computing various statistics, and finally computational complexity involved in solving for the efficient

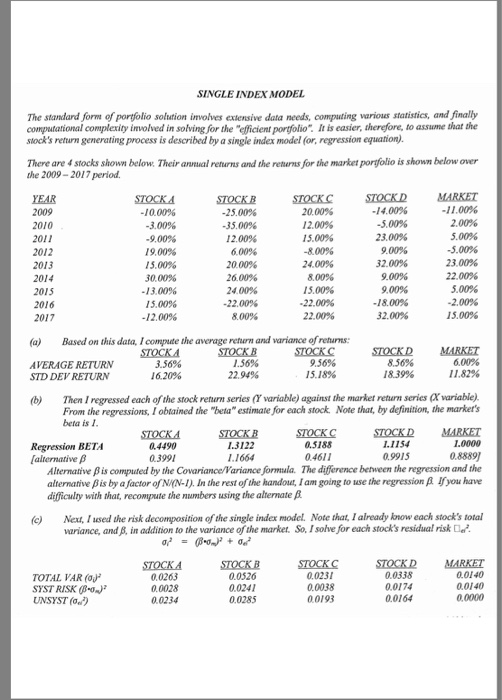

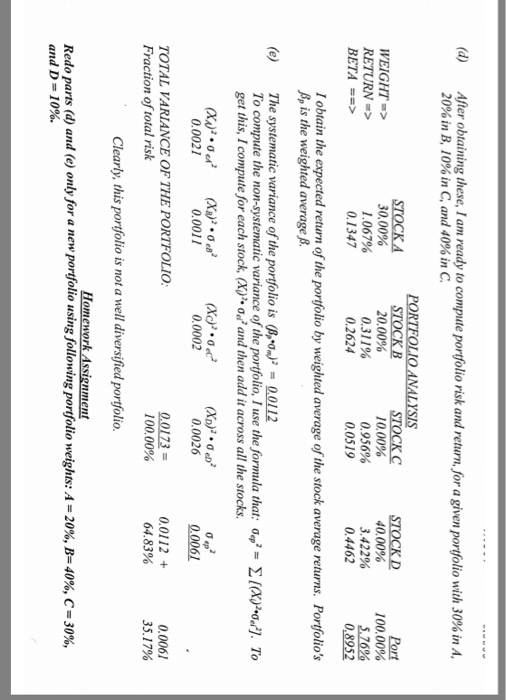

SINGLE INDEXMODEL The standard form of portfolio solution involves exiensive data needs, computing various statistics, and finally computational complexity involved in solving for the "efficient portfolio". It is easier, therefore, to assume that the stock's return generating process is described by a single index model (or, regression equation) There are 4 stocks shown below. Their annual returns and the retuns for the market portfolio is shown below over the 2009- 2017 period YEAR 2009 -10.00% -3.00% -9,00% 19.00% 15.00% 30, 00% 13 00% 15.00% -12.00% -35.00% 12.00% 6.00% 20 00% 26,00% 24.00% -22.00% 8.00% STOCKCSTOCKD -14.00% -5.00% 23.00% 9.00% 32.00% 9.00% 9.00% -18.00% 32.00% 20.00% 12.00% 15.00% -8.00% 24.00% 8.00% 15.00% -22.00% 22.00% MARKET -11.00% 2.00% 5.00% -5.00% 23.00% 22.00% 5.00% -2.00% 15.00% 2011 2012 2013 2015 2016 2017 (a) Based on this data, Icompute the average return and variance of returns STOCKC 9.56% 15.18% STOCKD MARKET 6,00% 1 1.82% AVERAGE RETURN 3.56% 16.20% 1.56% 22.94% STD DEV RETURNN 18.39% (b) Then I regressed each of the stock return series ( variable) against the market retuarn series(X wariable). From the regressions, I obtained the "beta" estimate for each stock. Note that, by definition, the market's beta is I STOCKDMARKET 1.0000 Regression BETA 0.4490 0.399 1.3122 1.1664 0.5188 04611 1.1154 .9915 Alternative ? is computed by the Covariance/Variance omtala. The diference between the regression and the alternative ? is byafactoro NON-1). In the rest ofthe handout I am going to use the regression ? Ifyou have difficulty with that, recompute the numbers using the alternate B (c) Ne, I used the risk decomposition of the single index model. Note that, I already know each stock's total wariance, and B, in addition to the variance of the market. So, I solve for each stock's residual risk De TOTAL VAR (o SYST RISK UNSYST ( 0.0263 0.0028 0.0234 STOCK B 0.0526 0.0241 0.0285 0.0231 0.0038 00193 STOCKD MARKET 0.0140 00140 0.0000 0.0338 0.0174 0.0164

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts